COMMENTARY BY TREY FREEMAN

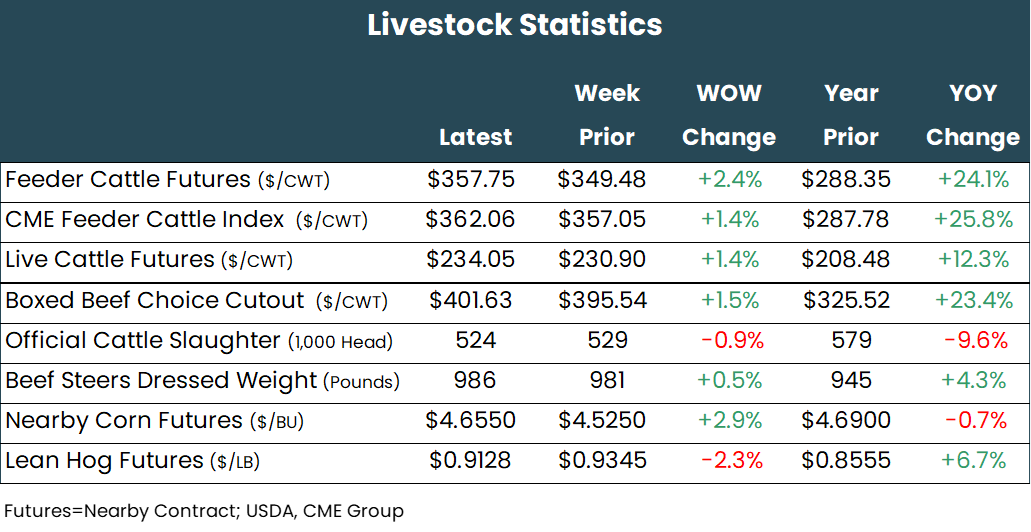

Cash fed cattle trade developed on Friday at $235 per hundredweight in both the North and South, in line with last week. Dressed trade in the North was also steady at $372 per hundredweight.

This week’s slaughter was much lighter than expected at 508,000 head, 17,000 fewer head week-over-week and 50,000 fewer than a year ago. Initial expectations were closer to 525,000.

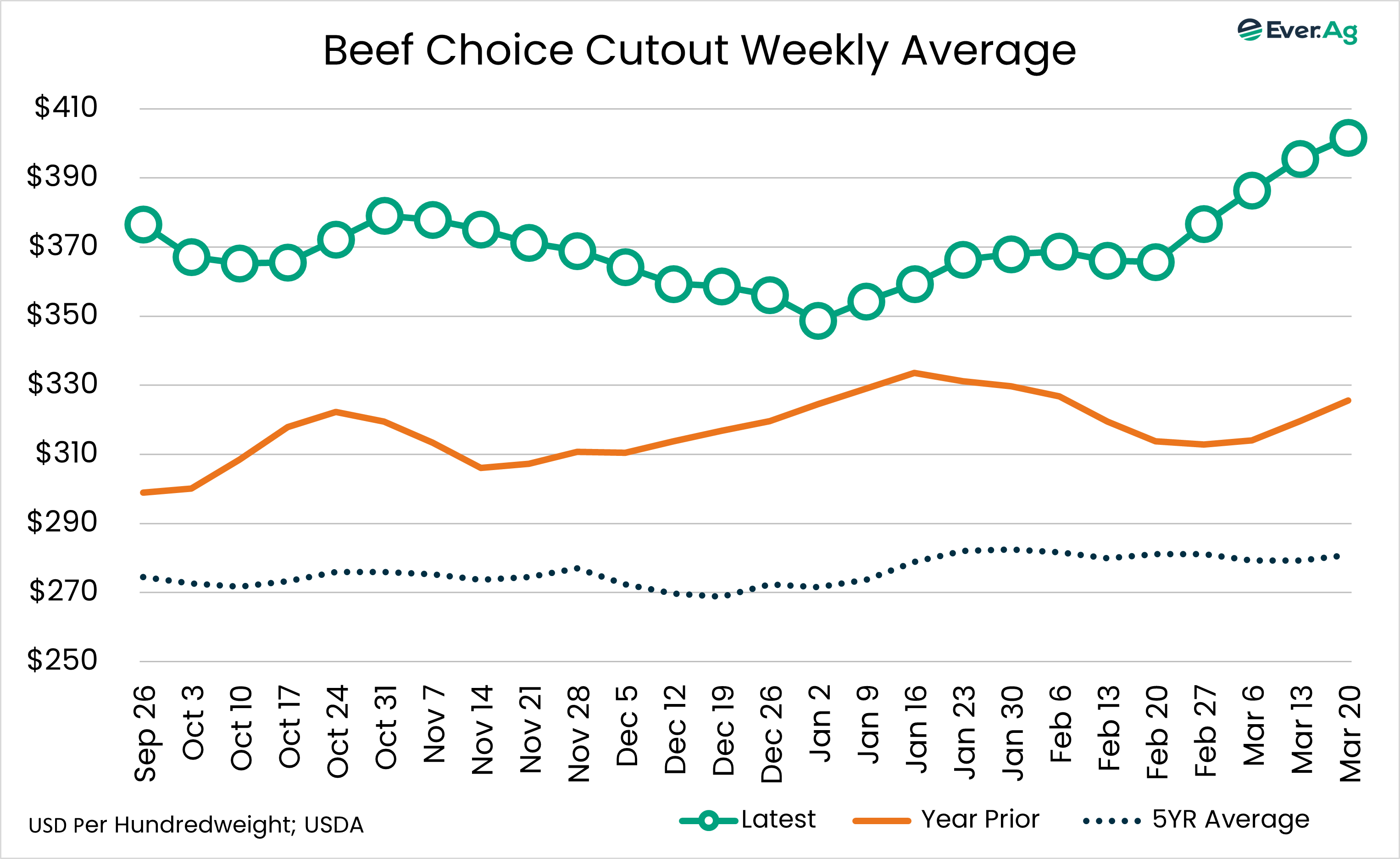

Tight kills helped push boxed beef cutout higher again, with choice up $2.19 per hundredweight to $400.11 and select up $1.40 to $391.54.

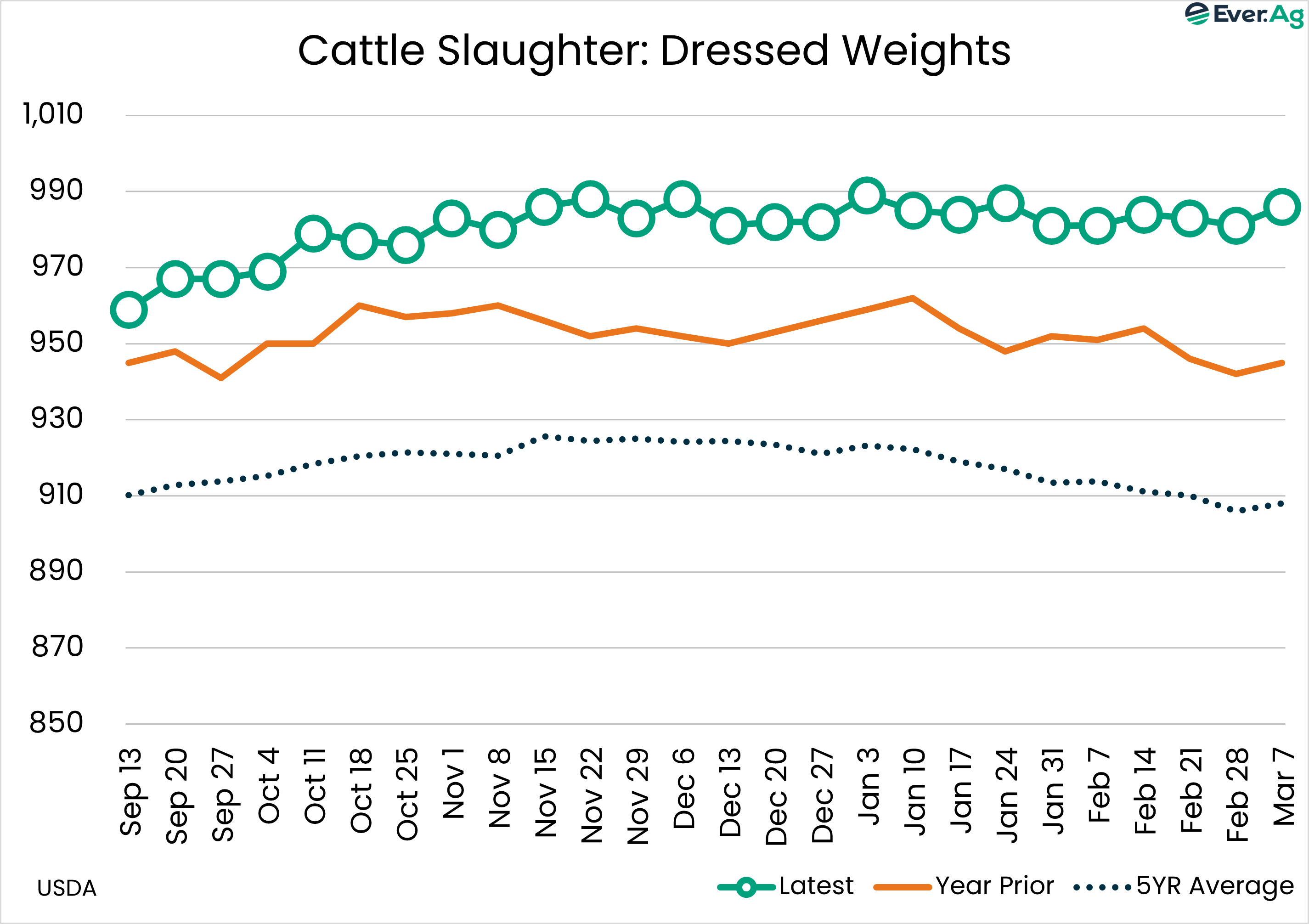

Official slaughter data released Thursday for the week ending March 7 showed dressed steer weights up five pounds from the week prior to 986 pounds. Dressed heifer weights rose ten pounds to 901 pounds, a new record, beating the previous record of 900 pounds from early January.

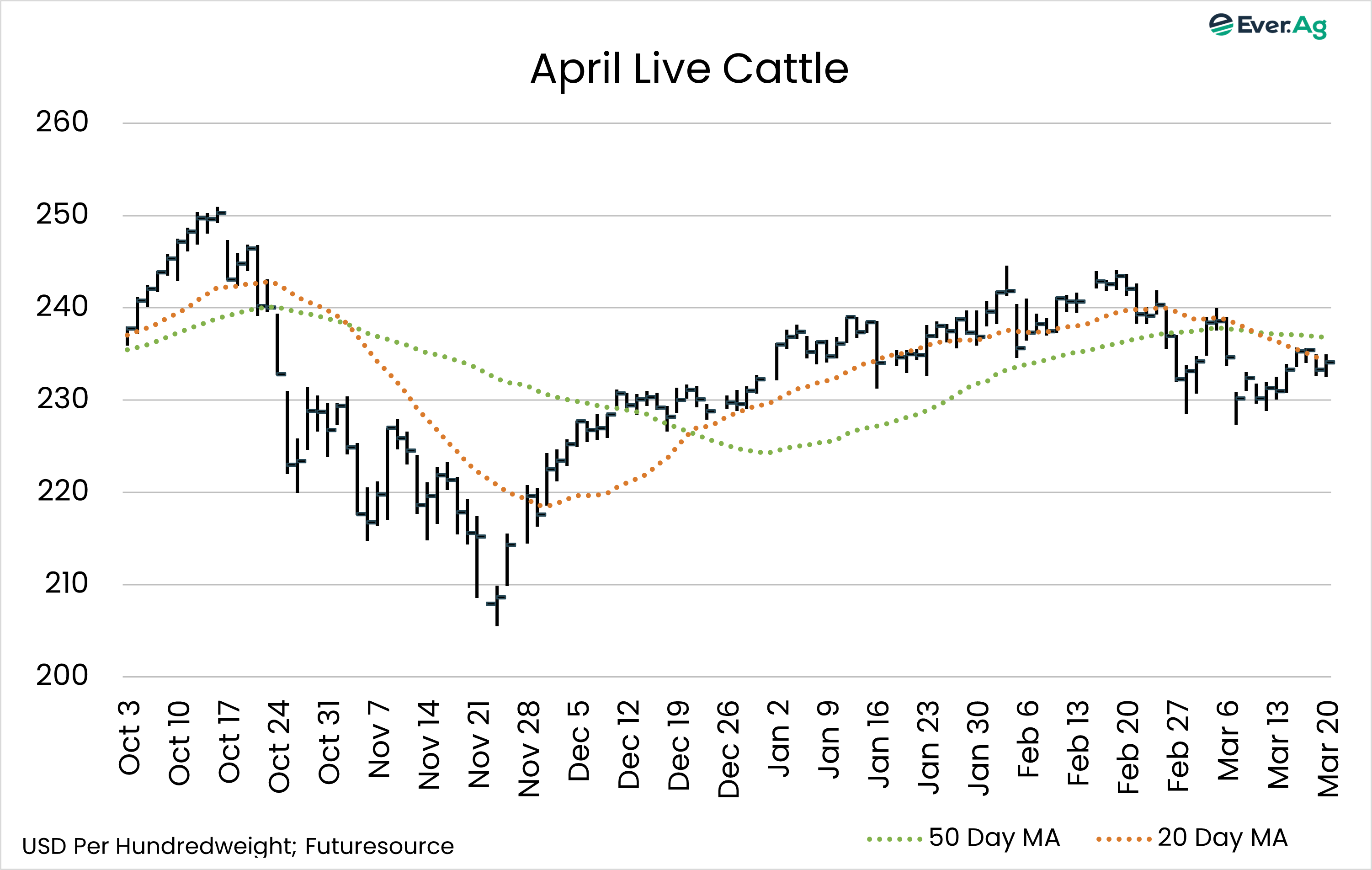

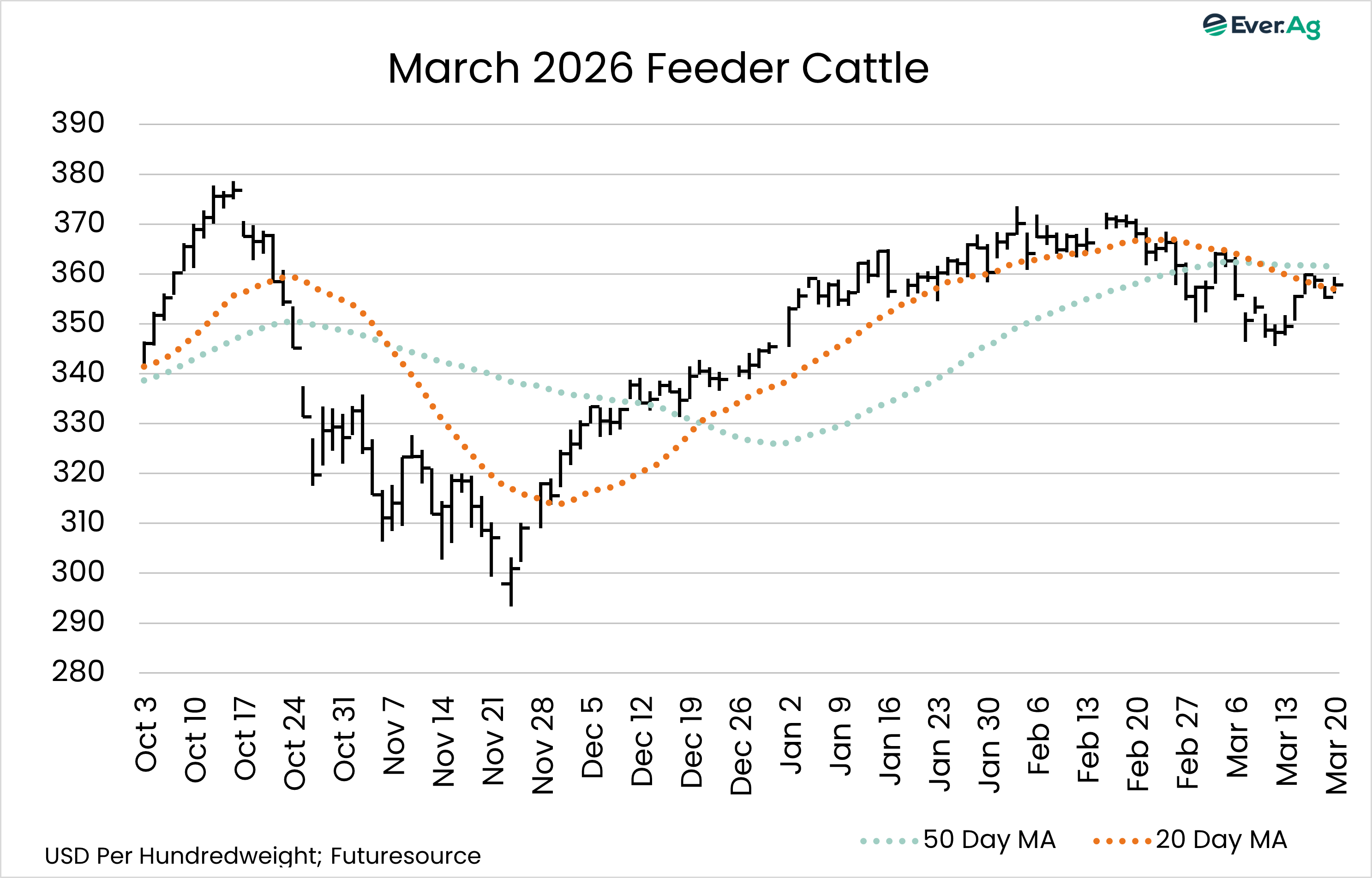

Geopolitical uncertainty continues to rattle equity markets, along with commodities in general. Despite the turmoil, cattle futures managed to finish the week with gains. April live cattle finished with a gain of $3.150 per hundredweight. June through December live cattle rose $3.025 to $4.475, with the greatest increases in the nearby contracts. Feeder cattle futures finished with gains of $6.450 to $8.275 per hundredweight, with the greatest gains in the nearby contracts. Open interest in live cattle remains relatively flat, increasing only a few hundred contracts through Thursday.

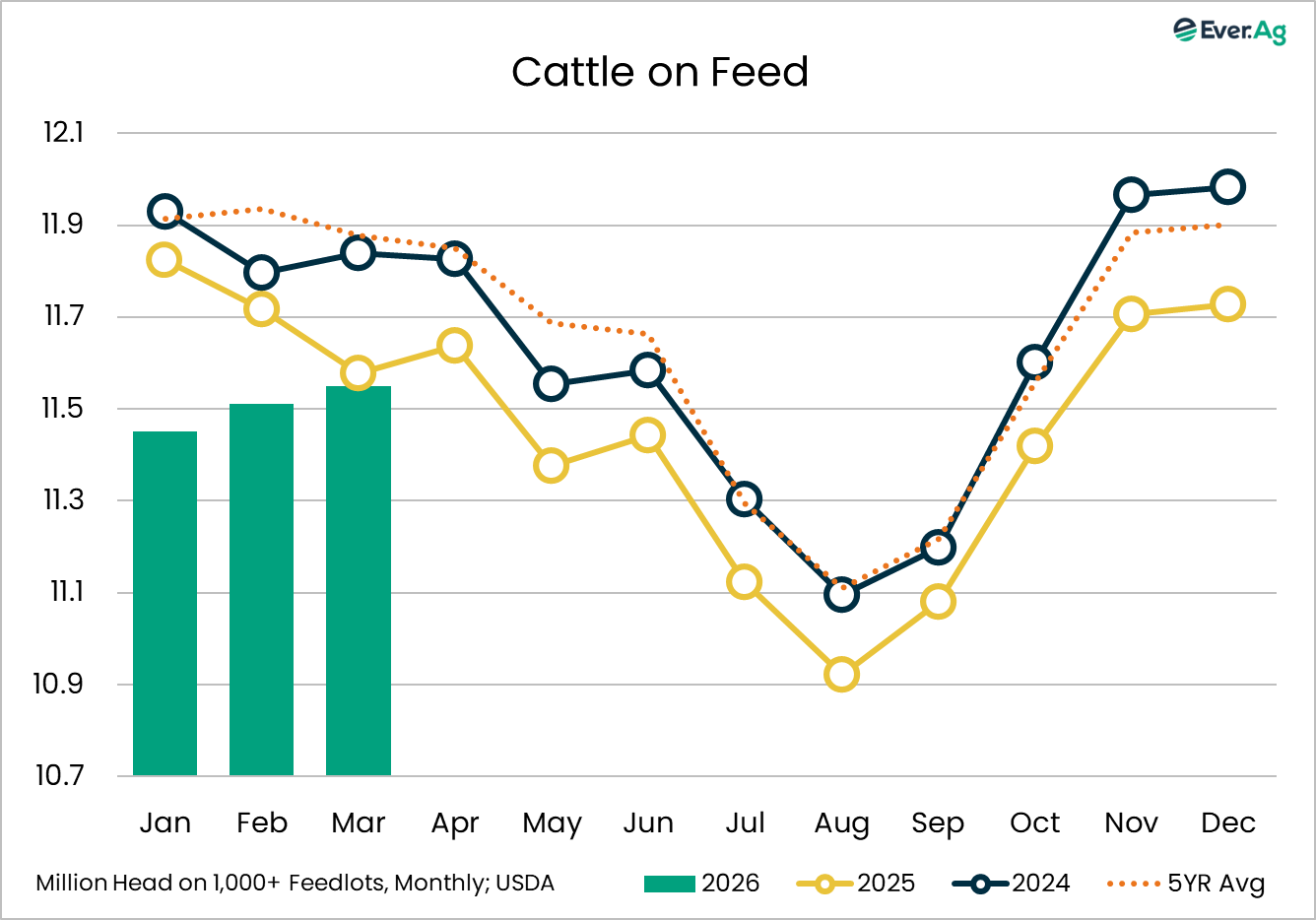

Today’s monthly Cattle on Feed report was mostly in line with pre-report expectations, although placements were slightly higher than anticipated. The number of cattle on feed as of March 1 was 99.8% of a year ago versus analysts’ expectations of 99.3%. Placements in February were 103.7% of a year ago compared to the pre-report estimate of 100.3%. The higher-than-expected placements number may paint a slightly bearish tone; however, it still fell within the range of estimates from 96.3% to 105%. Cattle marketed in February was 93.2% of a year ago, higher than the pre-report estimate of 92.4%.

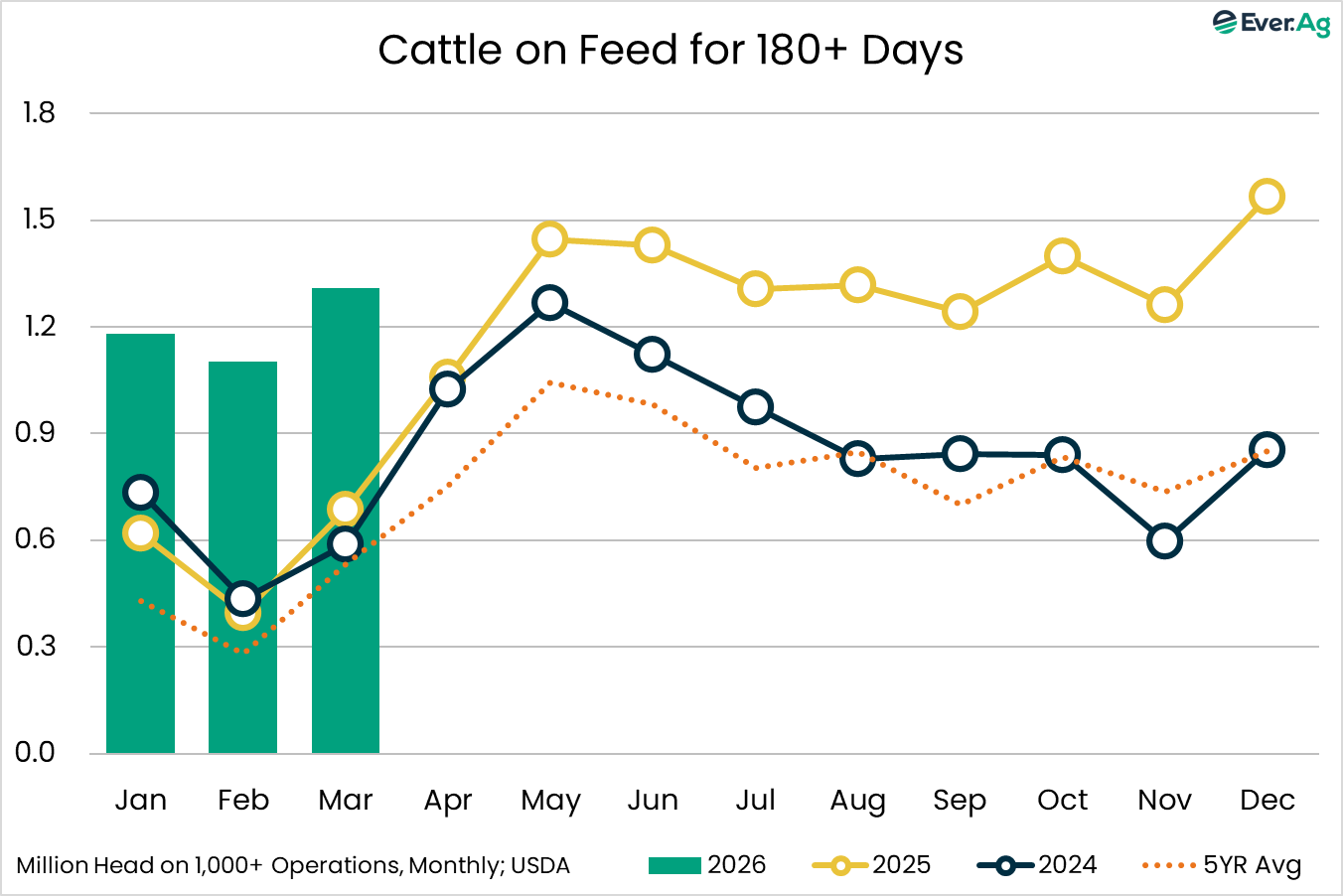

An ongoing concern of the market going back several months now is the growing number of cattle on feed with more than 150 days. As of March 1, this number is 18% higher than a year ago, or about 490,000 more head. For cattle on feed for more than 180 days, this number is 91% higher than a year ago, or about 620,000 more head. The extremely light kills through the first part of the year warrants caution as to what extent cattle are being backed up and when the market will have to deal with the matter.

Absent any negative headlines on the geopolitical front over the weekend, live and feeder cattle futures will likely be quick to turn focus back to the cash and beef markets on Monday. With packer margins back in the black, futures should have a level of support underneath them. Slaughter is expected to jump up to levels around 550,000, which has not been seen since mid-January. Boxed beef cutout values stalled toward the end of the week, likely a function of next week’s anticipated increase in production. With Spring beef demand still a month away, packers are likely to keep a tight rein on slaughter, with only slight allowance for increased kills until then.

Futures and options on futures trading involve significant risk and are not suitable for every investor. Information contained herein is strictly the opinion of its author and not necessarily of Ever.Ag and is intended for informational purposes. Information is obtained from sources believed reliable but is in no way guaranteed. Opinions, market data and recommendations are subject to change at any time. Past results are not indicative of future results. Trey Freeman and Matt Wolf maintain financial interests in the commodity contracts mentioned within this research report at the time it is published. Reproduction or redistribution is prohibited by law. Ever.Ag Insurance Services is an affiliate of Ever.Ag and is a licensed insurance agency in the following states: AZ, CA, CO, CT, FL, GA, ID, IL, IN, IA, KS, KY, LA, ME, MD, MA, MI, MN, MO, MT, NE, NV, NH, NM, NY, NC, ND, OK, OH, OR, PA, RI, SD, TN, TX, UT, VT, VA, WA, WV, WI, WY. This agency is an equal-opportunity employer.