COMMENTARY BY ABBY GREIMAN

Multiple headwinds pressured cattle markets this week, driving sizable week-over-week losses. The headline story continues to be the potential strike at the JBS beef packing plant in Greeley, CO. Two weeks ago, union members at the plant voted to authorize the strike but then went back to the table to negotiate. Those negotiations now appear to have stalled, prompting the union to register members for a strike this week. The Greeley JBS plant is one of the largest fed beef plants in the US, and a shutdown would quickly disrupt cattle and beef movement, even if taken offline for just a short period. Reduced packer competition for cattle would likely pull cash prices lower.

Global uncertainty, particularly the situation between the US and Iran, added pressure to markets this week. Indices and stock markets were in the red, which can bleed over into cattle markets. In addition, the end of the week coincided with month end. Both these factors can lead to managed-money profit taking and broader risk-off positioning, which brings selling pressure to the market. Combined, these forces drove this week’s market weakness.

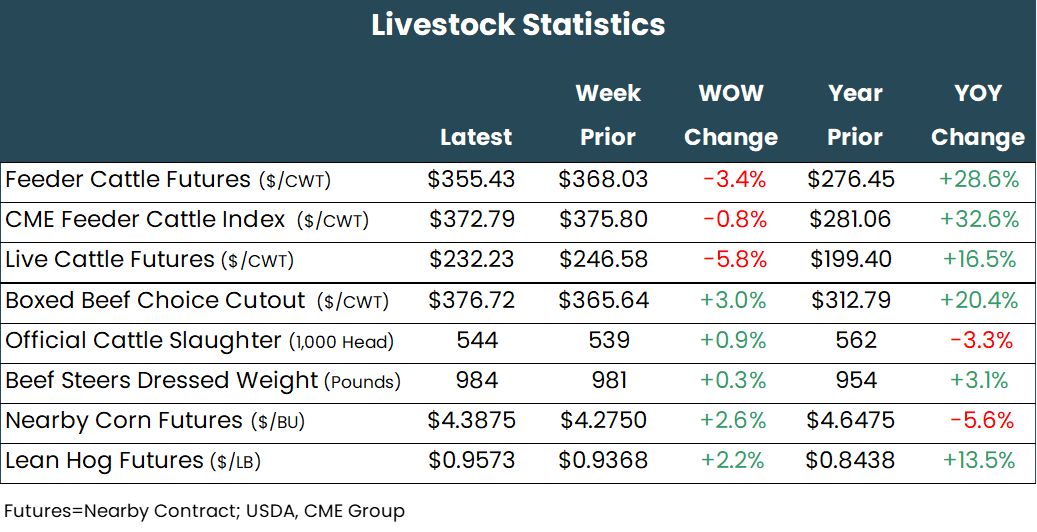

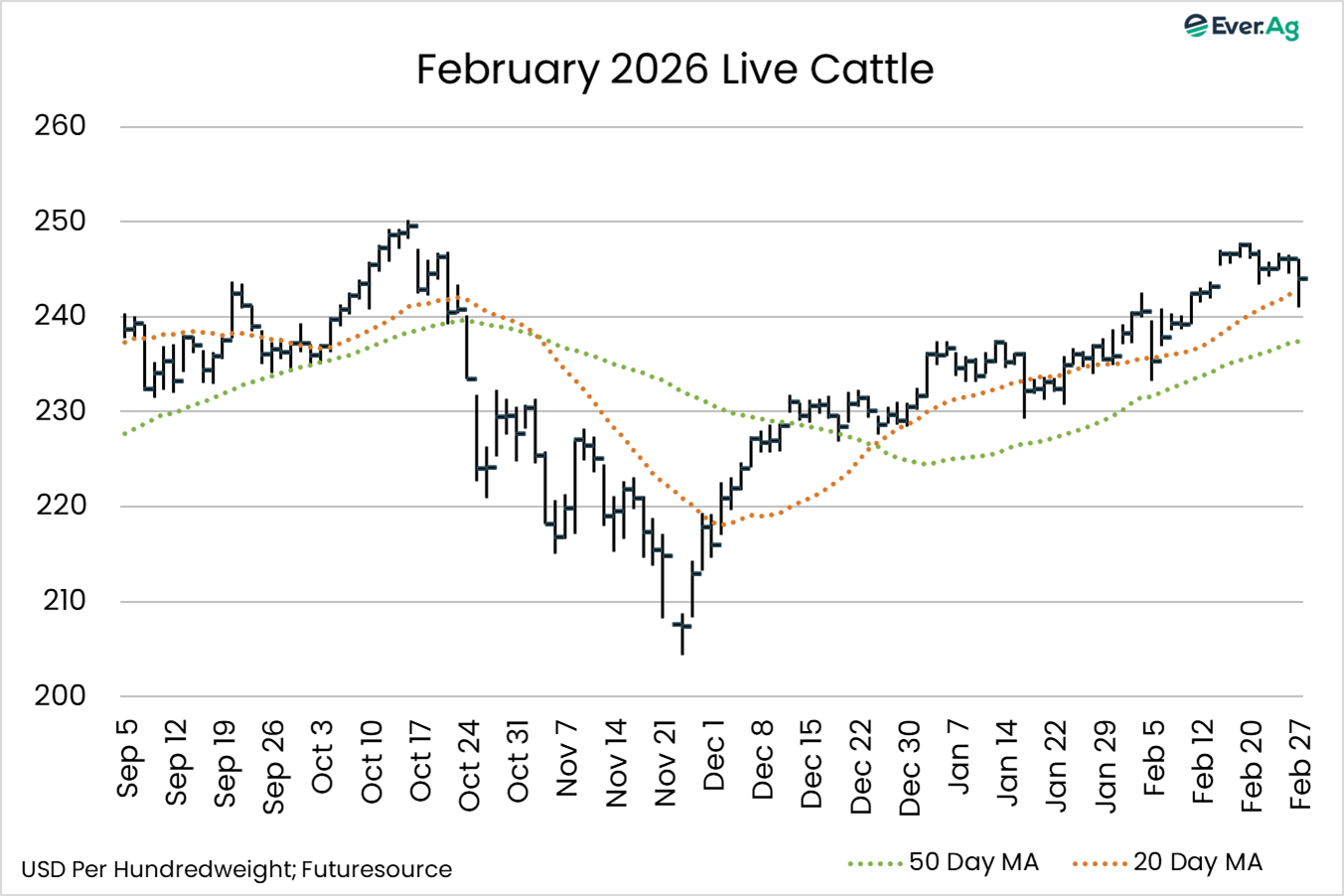

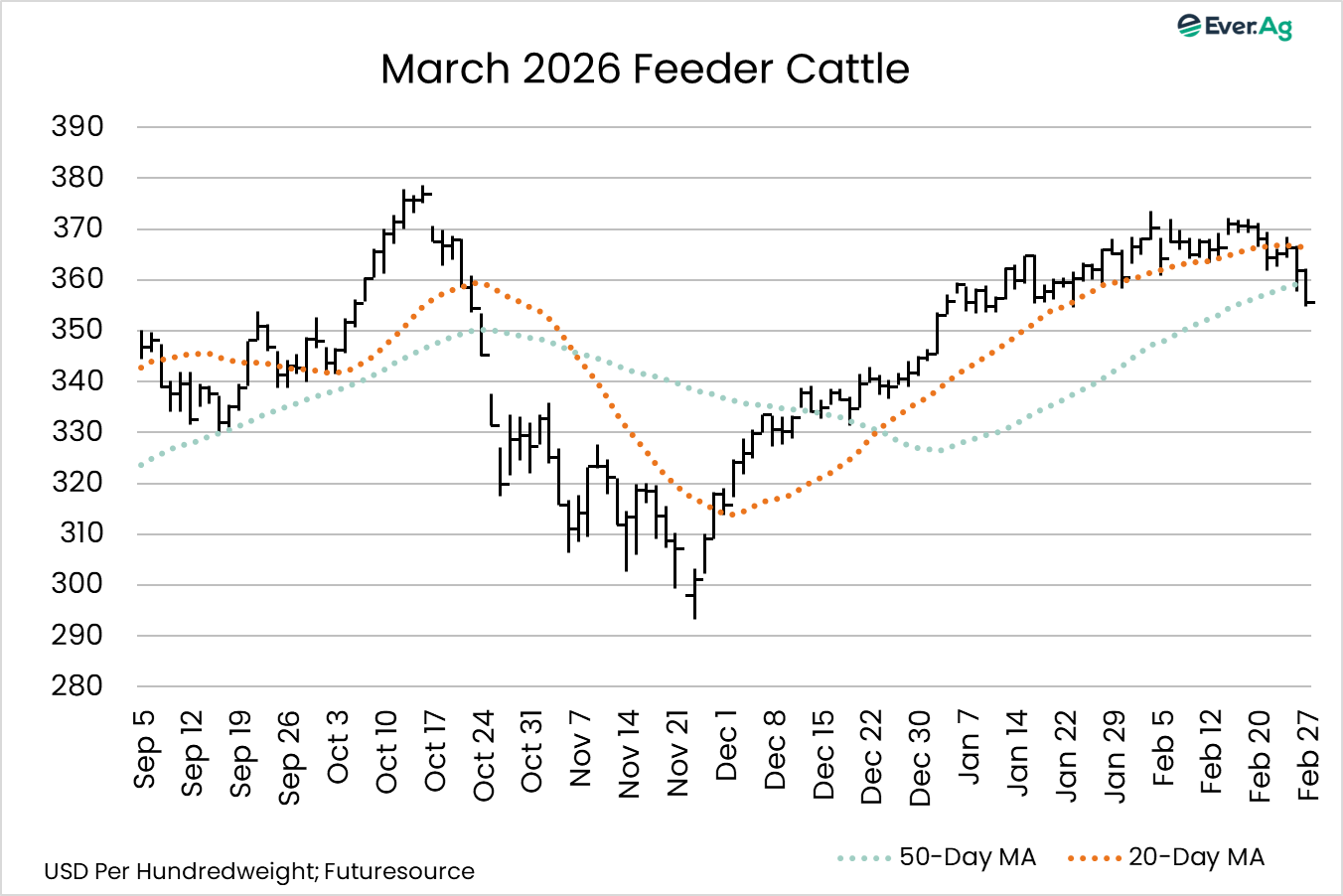

Live cattle front month February went off the board on Friday at $244.00 per hundredweight, down $2.575 week-over-week. The deferred months suffered more, with the April through August contracts down $7.175 to $9.775. Front month April now leads the board, settling Friday at $232.225 per hundredweight, a notable discount to current cash trade. Feeder cattle front month March finished the week at $355.425 per hundredweight, down $12.60 week-over-week, while the April through September contracts were down $13.10 to $13.85.

Futures action this week offered packers some margin relief, with cash trade lower than last week. Northern trade occurred around $243 per hundredweight, down $2 to $3 from last week. The south traded at $244, down $4 to $5 from last week. Cash feeder cattle trade also slowed, with the index at $372.79 on Friday, down from the all-time high set last Friday at $377.37. Early week auctions will likely see lower prices.

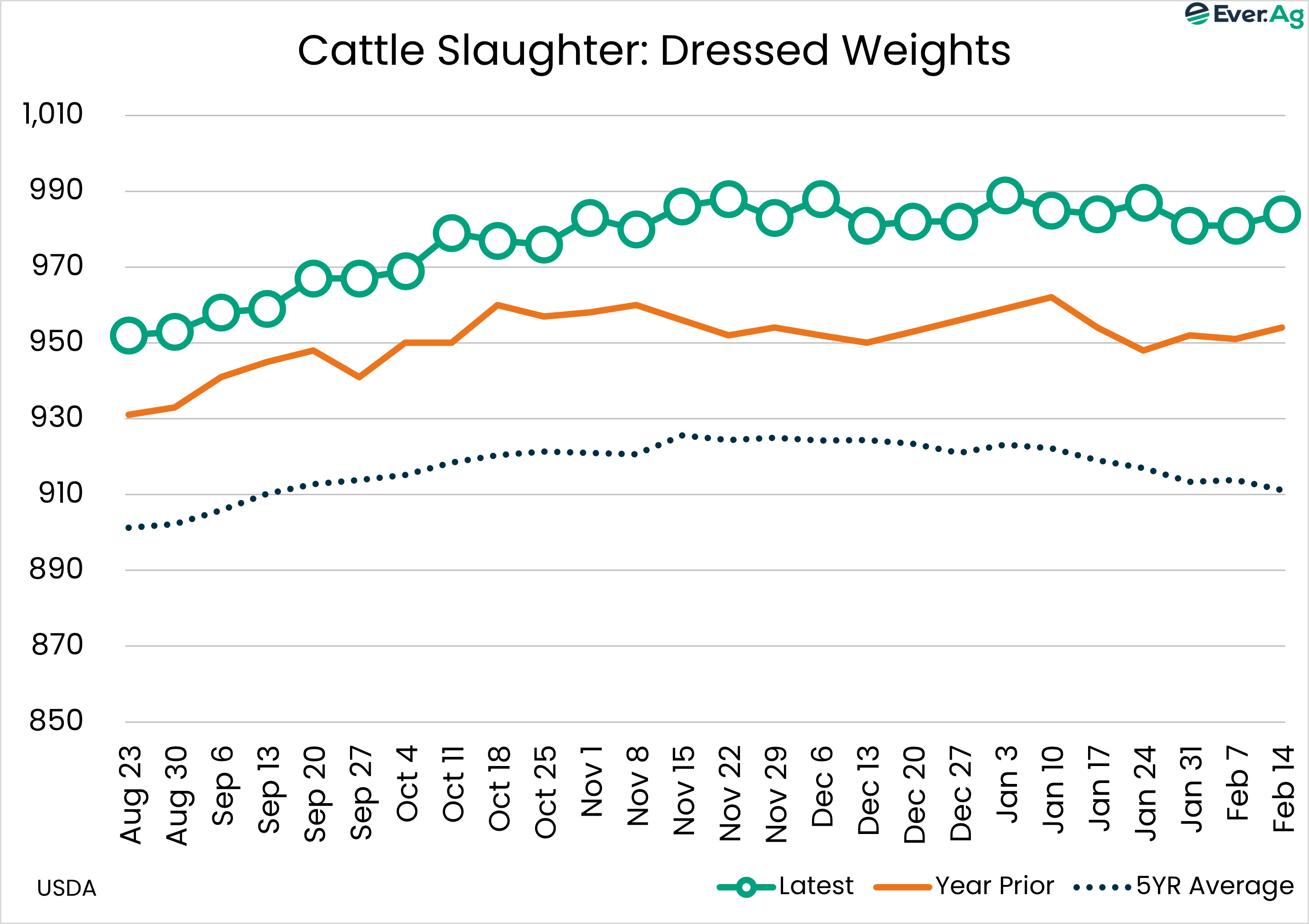

Weekly slaughter started the week stronger but finished at 516,000 head, right on par with last week. This compared to 569,000 head last year. Plants have already reduced hours, with some operating just four days per week. Industry chatter suggests additional unionized plants could soon run up against hour minimums, which would likely limit the potential for kill to be curtailed even more. Even with the slight improvement in margins this week, packers appear to be heading towards a situation in which change will be inevitable.

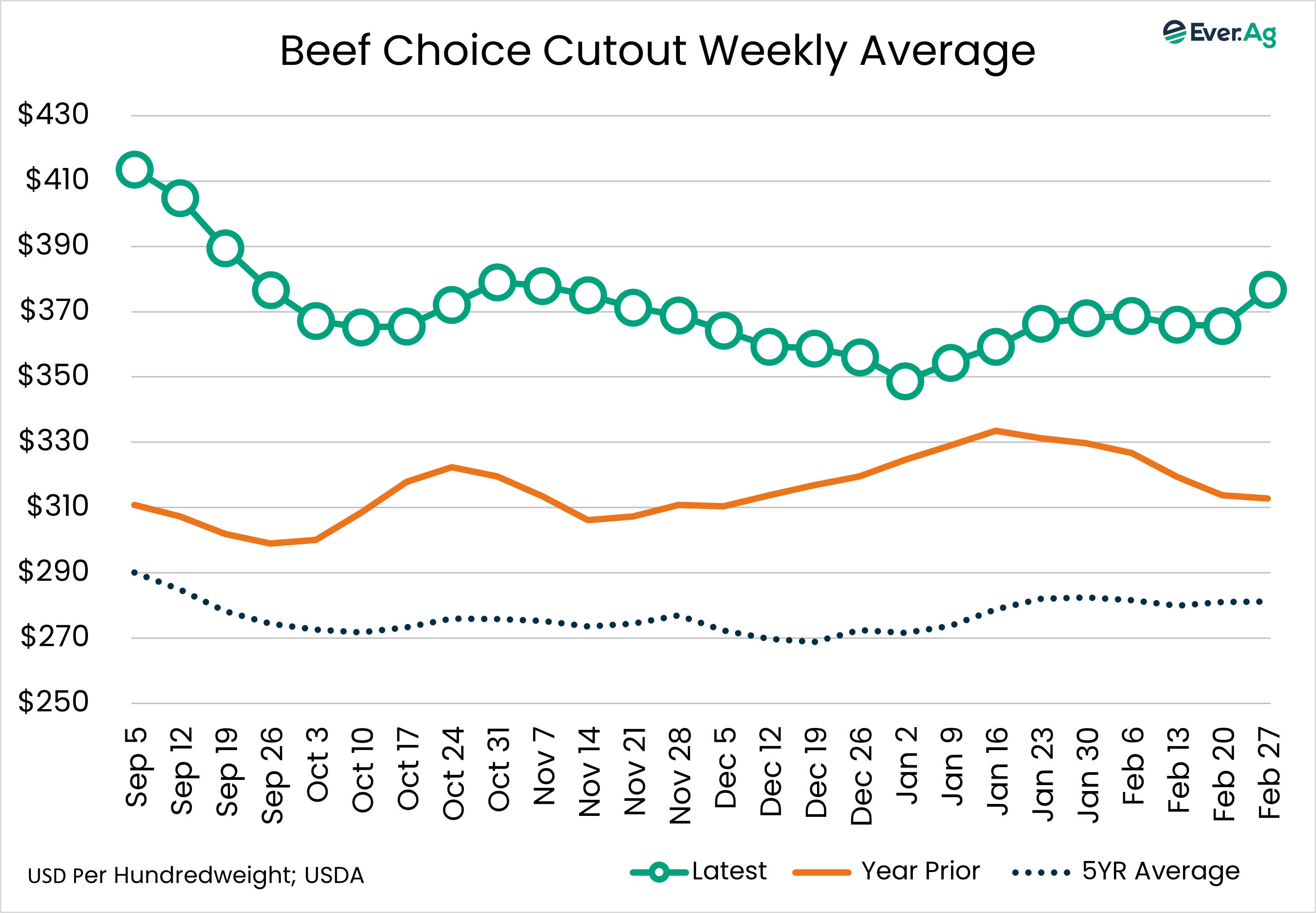

Sharply lower kills fueled a strong rally in cutout values, and an $8.21 jump in the Choice cutout headlined that rally. Ultimately, the Choice cutout ended up $13.07 per hundredweight week-over-week, while Select was up $13.51. The rib has been the driver of the Choice cutout lately, but this week, other primals started pulling their weight, with the loin and brisket gaining the most this week.

Higher cutout values helped improve margins, which could result in a slightly larger kill next week. However, every time there has been an improvement in margins and subsequent increase in kill lately, cutout strength faded quickly, prompting packers to scale back kills again. Slaughter will likely hold near 530,000 head or less until we start to get some seasonal traction back in the cutout.

This week serves as a reminder of the importance of risk management, even in a market that appears fundamentally set up for higher prices for some time to come. Will the market bounce back from this? Most likely. Are there new highs still out there in this cycle? Potentially. But there will also most definitely be other weeks, or maybe months, where outside factors impact futures markets, and thus cash markets as well. As a producer, marketing timelines are not always flexible to the point of avoiding the lows. Risk management can be a great tool to help smooth out the cattle industry’s current roller coaster ride.

Futures and options on futures trading involve significant risk and are not suitable for every investor. Information contained herein is strictly the opinion of its author and not necessarily of Ever.Ag and is intended for informational purposes. Information is obtained from sources believed reliable but is in no way guaranteed. Opinions, market data and recommendations are subject to change at any time. Past results are not indicative of future results. Trey Freeman and Matt Wolf maintain financial interests in the commodity contracts mentioned within this research report at the time it is published. Reproduction or redistribution is prohibited by law. Ever.Ag Insurance Services is an affiliate of Ever.Ag and is a licensed insurance agency in the following states: AZ, CA, CO, CT, FL, GA, ID, IL, IN, IA, KS, KY, LA, ME, MD, MA, MI, MN, MO, MT, NE, NV, NH, NM, NY, NC, ND, OK, OH, OR, PA, RI, SD, TN, TX, UT, VT, VA, WA, WV, WI, WY. This agency is an equal-opportunity employer.