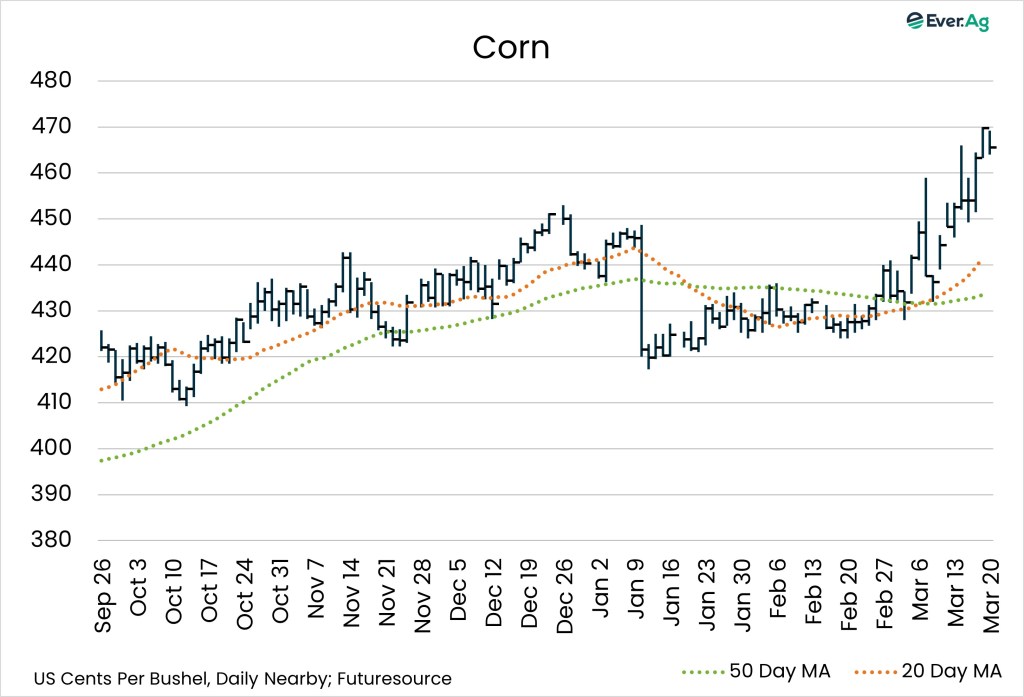

Corn

- The May corn contract settled at $4.6550 per bushel, nearly two cents lower on the week. July futures finished Friday at $4.7600 per bushel, down more than two cents.

- Ethanol production declined to 1.093 million barrels per day, down 2.9% on the week and -1.1% year-over-year. Stocks rose to 26.407 million barrels, up 3.2% week-over-week, but down 0.6% versus 2025.

- Old-crop US corn export sales were at the upper end of expectations at 1.172 million metric tons. With 12,000 metric tons sold, 2026-27 crop sales were at the lower end of the predicted range. Accumulated exports advanced to 1.711 billion bushels, ahead of the five-year average of 1.046 billion.

CORN COMMENTARY BY MEG JOHNSTON

- Recent geopolitical tensions injected additional volatility into the grain markets, supporting prices through higher energy prices and renewed uncertainty around global supply chains. With the recent rally in corn futures, farmers have been active sellers, taking advantage of higher prices. As a result, basis levels across the Midwest have softened somewhat in response to the futures strength.

- Old-crop corn contracts continue to trade below the $5.00-per-bushel mark, while December futures are hovering near that level. Meanwhile, March through July 2026 contracts have pushed above the $5.00 threshold, signaling some forward strength in the market.

Soybeans

- May soybeans closed at $11.6125 per bushel, down more than 76 cents week-over-week. The July contract ended the week at $11.7650 per bushel, 61 cents lower.

- For the week ending March 12, 2025-26 crop export sales totaled 298,208 metric tons, below predictions. New-crop sales were at the lower end of the expected range, with 6,600 metric tons sold. Accumulated soybean exports reached 1.031 billion bushels, behind the five-year average of 1.548 billion.

SOY COMMENTARY BY JON BAHR

- To start the week, we saw old-crop soybeans fall 70 cents on Monday. Representatives from the US and China met in Paris last weekend, and China told the US that they were done buying soybeans until Fall. Therefore, the 8 million metric tons of extra soybeans they were “considered” buying back at the beginning of February are off the table. China did tell the US they would still be willing to take 25 million metric tons for the next three crop years, which caused new-crop soybeans to claw back a good portion of Monday’s setback.

- Soybean exports remain disappointing. Old-crop weekly sales were below the expected range and new-crop came in at the lower end of predictions. This is not a surprise, as exports were lacking before we started trading over $12 futures on old crop. The big question is, “What is going to change the attitude of these export sales?”

- Exports are weak and funds as of last Friday were aggressively long, but fundamentals still say we are overpriced. The market is waiting to see if we have any surprises in USDA’s Prospective Plantings report coming up on March 31. For now, this to me is still a selling rally. At least look at downside put protection, because things can change in a hurry.

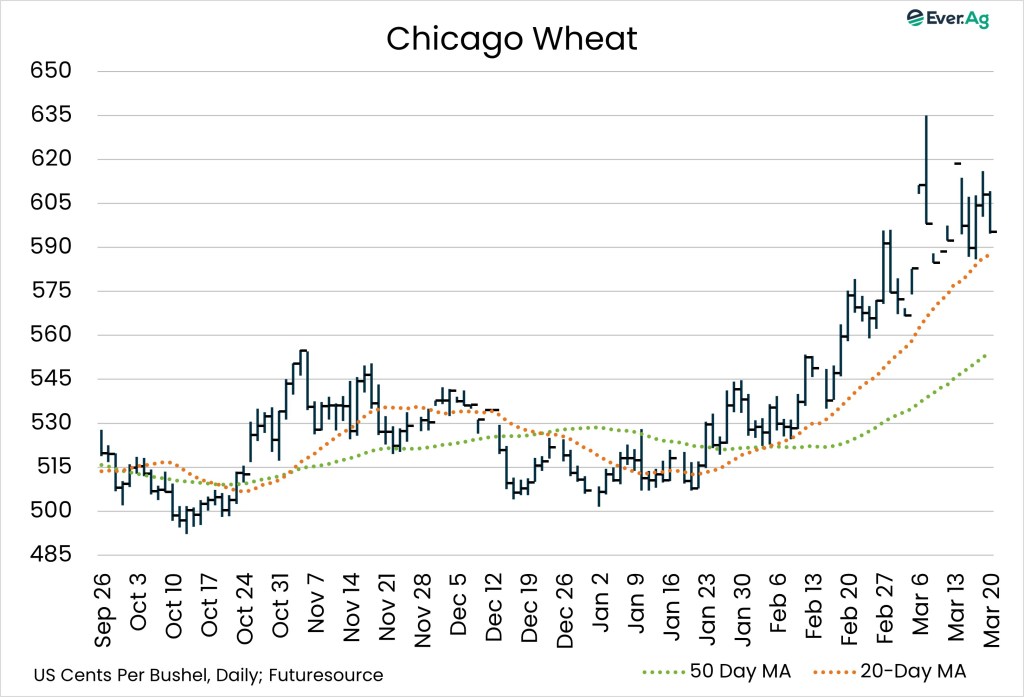

Wheat

- Nearby wheat futures finished Friday at $5.9525 per bushel, more than 23 cents lower on the week.

- Old-crop wheat export sales were below the predicted range at 189,887 metric tons. New-crop sales totaled 212,059 metric tons, above expectations. Accumulated exports reached 702.8 million bushels compared to the five-year average of 572.4 million.

WHEAT COMMENTARY BY NATALIE MCCARTY

- Much of the US is expected to be dry over the next couple weeks. In the Southern Plains, record-high temperatures will accompany the lack of moisture, exasperating the current drought situation. Currently, over 55% of the US winter wheat crop is impacted by drought. This week’s percentage of crop ratings in very poor and poor/fair condition categories are looking grim, with Texas at 85%, Oklahoma 82% and Kansas at 48%. These states need a drink of water to help the maturing crop.

- On top of this, a war continues to rage on, supporting the futures market. With the active military conflict in Iran stretching into week three, concern is mounting on how long this could go on. With energy and financial markets in turmoil, investors have been looking for a safer haven for their money and have piled into the grain markets. Index funds were the longest they had been in 13 months and were almost record long on Kansas City wheat this last week. This has added to the upward price momentum.

- Fundamentally, we still have ample supply of US and global wheat available. Early projections put wheat planting at 45 million acres versus last year’s 45.3.

Futures and options on futures trading involves significant risk and is not suitable for every investor. Information contained herein is strictly the opinion of its author and not necessarily of Ever.Ag and is intended for informational purposes. Information is obtained from sources believed reliable but is in no way guaranteed. Opinions, market data and recommendations are subject to change at any time. Past results are not indicative of future results. Jon Bahr maintains financial interest in the commodity contracts mentioned within this research report at the time it is published. Katie Burgess, John Billington, Kathleen Wolfley, Erica Maedke, Meg Johnston and Natalie McCarty do not maintain financial interest in the commodity contracts mentioned within this research report at the time of publication. This report is in the nature of a solicitation.