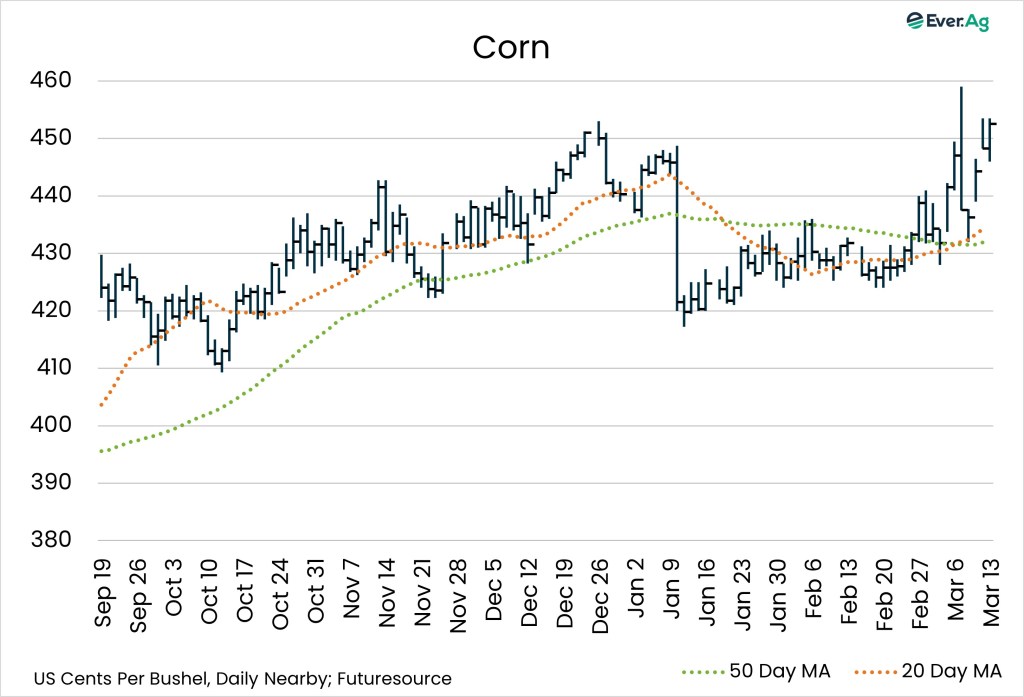

Corn

- USDA’s March WASDE report left US corn ending stocks at 2.127 billion bushels, unchanged on the month. That was slightly below predictions for 2.136 billion bushels.

- March corn closed at $4.5250 per bushel, 5.5 cents higher week-over-week. The May contract settled at $4.6725 per bushel, up almost seven cents.

- Ethanol production climbed to 1.126 million barrels per day, up 2.8% week-over-week and +6.0% on the year. Stocks slipped to 25.580 million barrels, down 2.9% on the week and -6.6% versus 2025.

- Old-crop US corn export sales totaled 1.503 million metric tons, within expectations. With 500 metric tons sold, 2026-27 crop sales were at the bottom end of the predicted range. Accumulated corn export sales reached 1.642 billion bushels compared to the five-year average of 982.51 million bushels.

CORN COMMENTARY BY BRANDON WEIGEL

- The war in Iran and subsequent increases in energy prices sent corn futures skyward this week as managed money rotated capital away from the equity markets and into commodities as “safe haven”/inflationary hedge assets.

- December corn futures started off the week on a hot note, hitting $4.9850 per bushel on Sunday evening as crude oil prices struck nearly $120 per barrel. The strong correlation between corn prices and crude oil prices is one that has a long-standing history and deserves to be watched closely.

- US FOB corn export values continue to trade at a premium to that of Argentina by about $12 per ton. Export sales for the week ending March 5, however, came in in the middle of the expected range.

- Mato Grosso Brazil reported sahfrina crop corn planting over 90% complete at the start of this week. Argentina corn good/excellent ratings also rank among the best in recent times.

- Meanwhile, fertilizer prices surged on the back of restricted passage through the Strait of Hormuz. That brought the discussion around acreage rotation back in full swing. Will producers with unpriced fertilizer consider rotating acres away from corn and into beans because of surging fertilizer prices?

- The recent price rally in corn has pulled most producers into profitable territory for 2026, especially for those that had locked fertilizer prices ahead of this current conflict.

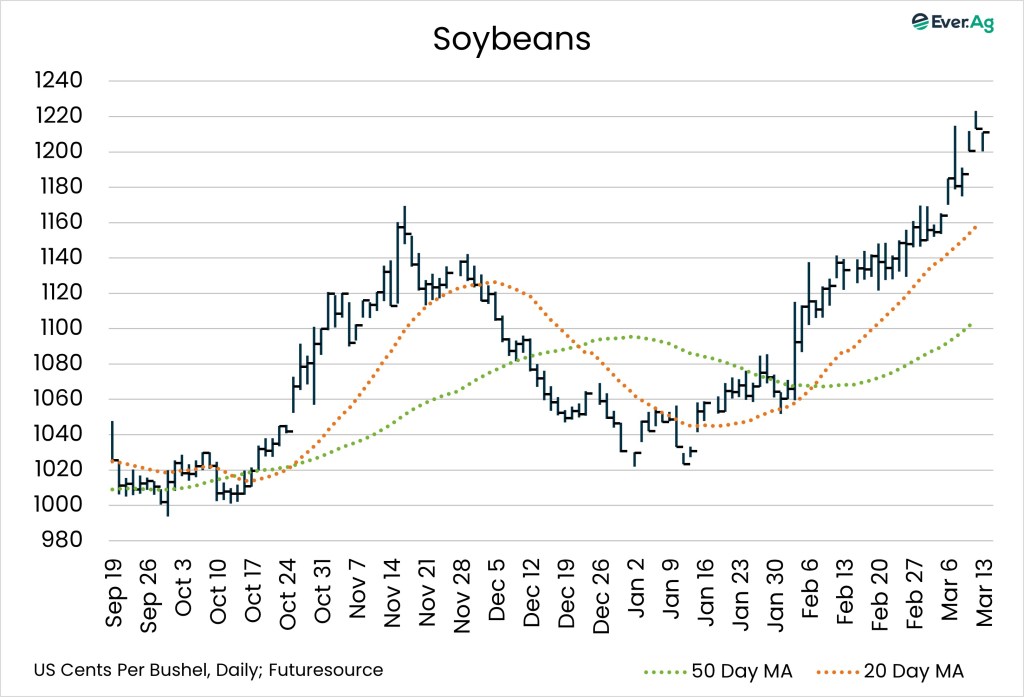

Soybeans

- US soybean ending stocks held steady month-over-month at 350 million bushels, just slightly ahead of expectations for 344 million.

- The March soybean contract ended the week at $12.1100 per bushel, up 26 cents versus the previous Friday. July soybeans closed at $12.3750 per bushel, 24.5 cents higher.

- US 2025-26 soybean crop export sales reached 456,740 metric tons, in the middle of the expected range. New-crop sales totaled 9,518 metric tons, at the lower end of predictions. With 997.55 million bushels sold, accumulated exports remain well behind 1.519 billion bushels on the five-year average.

SOY COMMENTARY BY JAKE KINGSLEY

- Soybeans continue their impressive rally, reaching new contract highs in both the old- and new-crop curves. The strength is in response to crude oil breaking $100 per barrel for the first time since 2022. With the reinvigorated renewable diesel program now pushing soybean oil futures to a strong correlation with crude oil futures, soy oil and soybean prices are following crude as the conflict in the Middle Ease unfolds.

- Excellent crush margins and recently added capacity have helped generate impressive domestic demand for soybeans. A large crop in 2025 followed by big production numbers coming from South America as they harvest their 2026 crop are keeping fundamentals steady, and March’s WASDE was neutral on comfortable ending stocks numbers.

- Analysts are having a tough time projecting the long-term trends in pricing with the day-to-day volatility, but some new news emerged. Cargill announced it is pausing soy shipments from Brazil to China due to changes in export inspection requirements. This poses a serious dilemma for Brazilian farmers who have limited storage capacity and are in the midst of harvesting one of the largest crops on record. The development could push more Chinese demand to US ports if buyers need the beans, but our prices are considerably higher at this time. Alternatively, if demand does not shift to the north, supply backing up into the Brazilian countryside will begin to pressure market prices lower as the supply chain looks to move product.

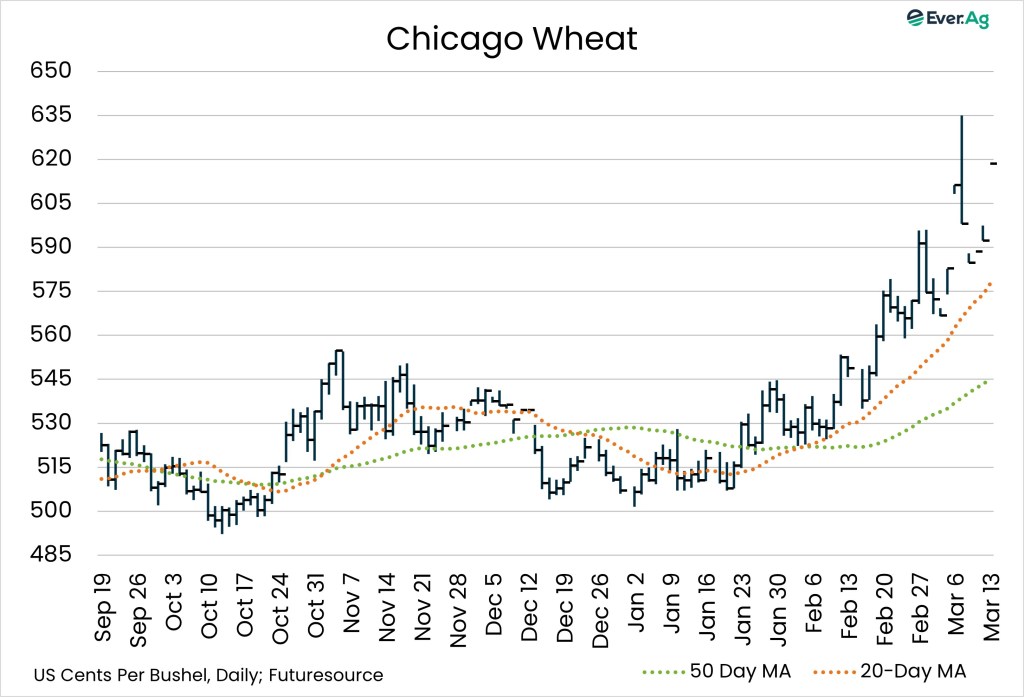

Wheat

- According to USDA, US wheat ending stocks were unchanged on the month at 931 million bushels, ahead of expectations for 926 million.

- Nearby wheat futures finished Friday at $6.1850 per bushel, more than seven cents higher week-over-week.

- Old-crop US wheat export sales reached 455,439 metric tons, above the predicted range. New-crop sales surpassed expectations, with 40,350 metric tons sold. Accumulated wheat exports totaled 688.7 million bushels, ahead of 556.7 million on the five-year average.

WHEAT COMMENTARY BY COLE WEINKAUF

- Wheat has seen a nice run over the last few weeks, but its rallies haven’t been as aggressive as other commodities in reacting to turmoil in the Middle East. Estimates put funds near flat. Global supply fundamentals are bearish, likely leading funds to avoid building a long position. Supply will return to the forefront once Iran war risks fade.

- Exports had a nice week, with outbound volume above the expected range. Russia’s rail operator expects March exports to reach 3.7 million tons, nearly double March 2025 and above the five-year average of 2.9 million. Russia is redirecting wheat exports to Iran via the Caspian Sea as Black Sea port terminals remain temporarily closed.

- Forecasts for the next two weeks call for a much drier weather pattern and increasing crop stress in the US Plains, especially in the southwest areas. There are no cold risks in the forecast through the end of the month.

- This week’s pullback seems to have run its course, but wheat has lost its leadership role from late last week. The near-term path of least resistance may still be higher, at least until the Iran situation stabilizes, but wheat will be quick to turn lower once geopolitical risk decreases.

Futures and options on futures trading involves significant risk and is not suitable for every investor. Information contained herein is strictly the opinion of its author and not necessarily of Ever.Ag and is intended for informational purposes. Information is obtained from sources believed reliable but is in no way guaranteed. Opinions, market data and recommendations are subject to change at any time. Past results are not indicative of future results. Brian Fletcher, Jon Spainhour, and Brandon Weigel maintain financial interest in the commodity contracts mentioned within this research report at the time it is published. Erica Maedke, Jake Kingsley and Cole Weinkauf do not maintain financial interest in the commodity contracts mentioned within this research report at the time of publication. This report is in the nature of a solicitation.