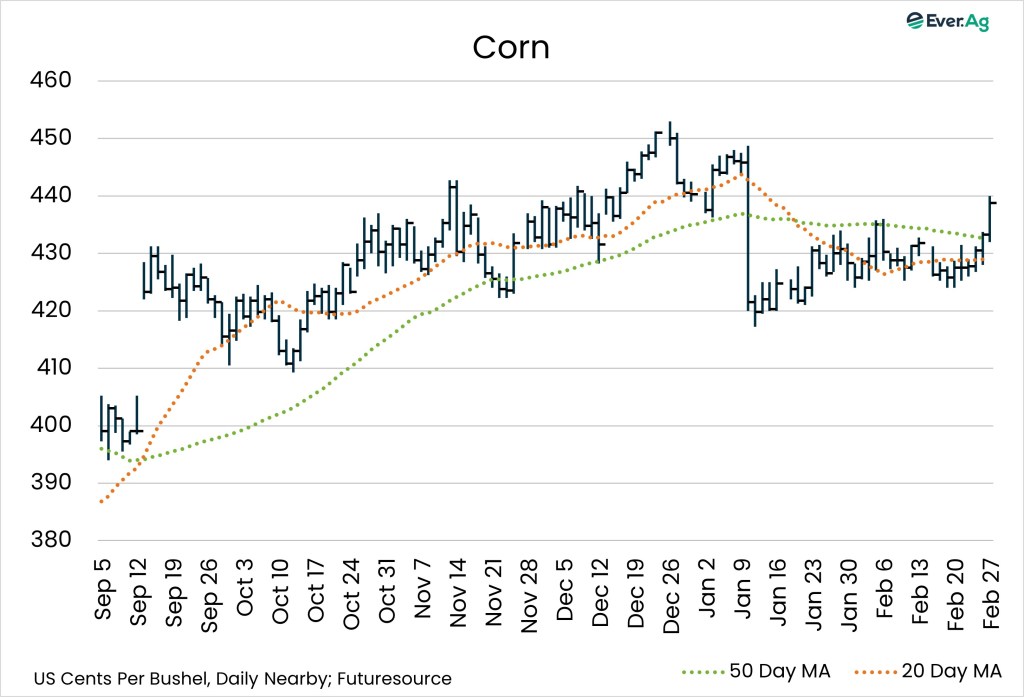

Corn

- The March corn contract closed at $4.3875 per bushel, more than 11 cents higher versus the previous week. May corn settled at $4.4850 per bushel, up nearly nine cents.

- Ethanol production totaled 1.113 million barrels per day, down 0.4% on the week, but up 3.0% year-over-year. Stocks reached 25.646 million barrels, up 0.2% week-over-week, but down 7.0% versus 2025.

- Corn export sales were slower for the week ending February 19. Old-crop sales were below the expected range at 685,804 metric tons, and 2026-27 crop sales were at the low end of predictions at 11,685 metric tons. Accumulated exports reached 1.509 billion bushels, ahead of the five-year average of 867.3 million bushels.

CORN COMMENTARY BY NATALIE MCCARTY

- The war for acres is on. New-crop corn has gone up over $0.20 per bushel, dragged higher by a soybean rally of over $0.70 per bushel that started because of talks about additional China soybean purchases. This seems unlikely, with harvest underway for South America’s large soybean crop and China/US relations still tense.

- This month, the new-crop soy/corn spread increased to 2.42, which typically is supportive of more corn acres. Last week, USDA projected that corn acres would go down from a record high of 98.8 million acres this year to 94 million for 2026-27. Soybeans were the main benefactor of the reported corn acreage drop. However, if this spread maintains or widens further, planting intentions could be modified.

- With tighter cash flow for many farmers this year, growers will be looking hard at input costs as a deciding factor of what to plant. Soybean input costs are lower than corn.

- While new-crop futures have had some excitement, old-crop futures increases have been much more tempered and rangebound. The large ending stocks number has kept a lid on pricing. Exports and ethanol production continue at a high level. This could cause a further ending stock reduction in the next WASDE report on March 10.

- Sign-up for USDA’s Bridge Payment Program is now open online or at local FSA offices. Deadline is April 17.

Soybeans

- March soybeans finished Friday at $11.5725 per bushel, up almost 20 cents on the week. The July contract closed at $11.8275 per bushel, nearly 17 cents higher.

- With 407,866 metric tons sold, 2025-26 crop soybean export sales were at the bottom end of expectations. There were no new-crop sales. Accumulated exports reached 919.8 million bushels, behind the five-year average of 1.448 billion bushels.

SOY COMMENTARY BY JENNI BIRKER

- The soybean market is navigating a mix of bullish and bearish forces this week. On the supportive side, South American weather is playing a dominant role. Argentina’s persistent dryness is pressuring soybean conditions, lending support to futures, especially as soybean meal strengthens on tightening production prospects. In contrast, Brazil’s crop remains strong, with production continuing to anchor heavy global supply.

- Trade policy remains a major swing factor. US tariff uncertainty stemming from the newly implemented 10% global tariff and the possibility of an increase to 15% has softened export potential, especially after soybean export inspections fell 45% from the prior week. However, there is a counterweight: the US and China’s extension of the “Busan Truce” includes China’s pledge to raise soybean imports to 20 million metric tons this year, with even larger annual commitments ahead. This has already triggered confirmed USDA “flash sales,” providing fundamental support.

- Domestically, soybean crush demand continues to trend above last year, a reflection of expanding processing capacity tied to renewable diesel growth. This demand helps offset export softness, though global oversupply keeps upward momentum in check.

- Overall, the soy market sits at a crossroads of weather-driven support, policy-driven uncertainty and structural biofuel-driven demand. The result? Choppy-but-firm price action as traders balance risk on both sides.

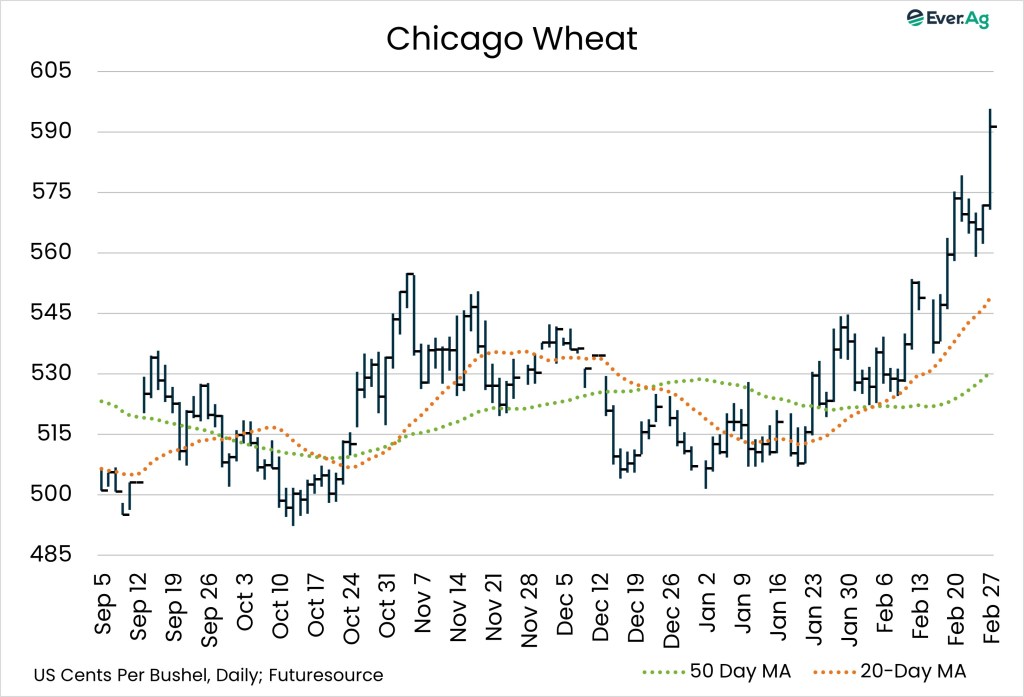

Wheat

- Nearby wheat futures settled at $5.9125 per bushel, almost 18 cents higher week-over-week.

- Old-crop wheat export sales were below expectations at 242,964 metric tons. But 2026-27 crop sales totaled 107,015 metric tons, above the predicted range. Accumulated exports reached 660.0 million bushels, ahead of the five-year average of 529.7 million bushels.

WHEAT COMMENTARY BY LORI NELSEN

- Wheat futures saw a nice rally this week, hitting an eight-month high before entering choppier waters. Black Sea conflicts and port disruptions, Argentine port strikes and the threat of winterkill in the US Great Plains are currently driving most of the wheat market action.

- Tariffs remain an unknown factor that could impact market direction. The Trump administration’s 15% global import tariff of agricultural goods has the market bracing for possible retaliation, which could disrupt existing wheat trade agreements. Argentina is expected to dominate markets in South America and Asia, crowding out US export opportunities.

- Meanwhile, the weather forecast in the US Plains is trending wet in early March. Unseasonably warm temperatures now risk prematurely breaking dormancy, making the crop more vulnerable to late freeze events. So, the market will have to keep an eye on the weather in that region.

Futures and options on futures trading involves significant risk and is not suitable for every investor. Information contained herein is strictly the opinion of its author and not necessarily of Ever.Ag and is intended for informational purposes. Information is obtained from sources believed reliable but is in no way guaranteed. Opinions, market data and recommendations are subject to change at any time. Past results are not indicative of future results. Brian Fletcher, Jon Spainhour, Jenni Birker and Lori Nelsen maintain financial interest in the commodity contracts mentioned within this research report at the time it is published. Kathleen Wolfley and Natalie McCarty do not maintain financial interest in the commodity contracts mentioned within this research report at the time of publication. This report is in the nature of a solicitation.