The Scoreboard

Comment

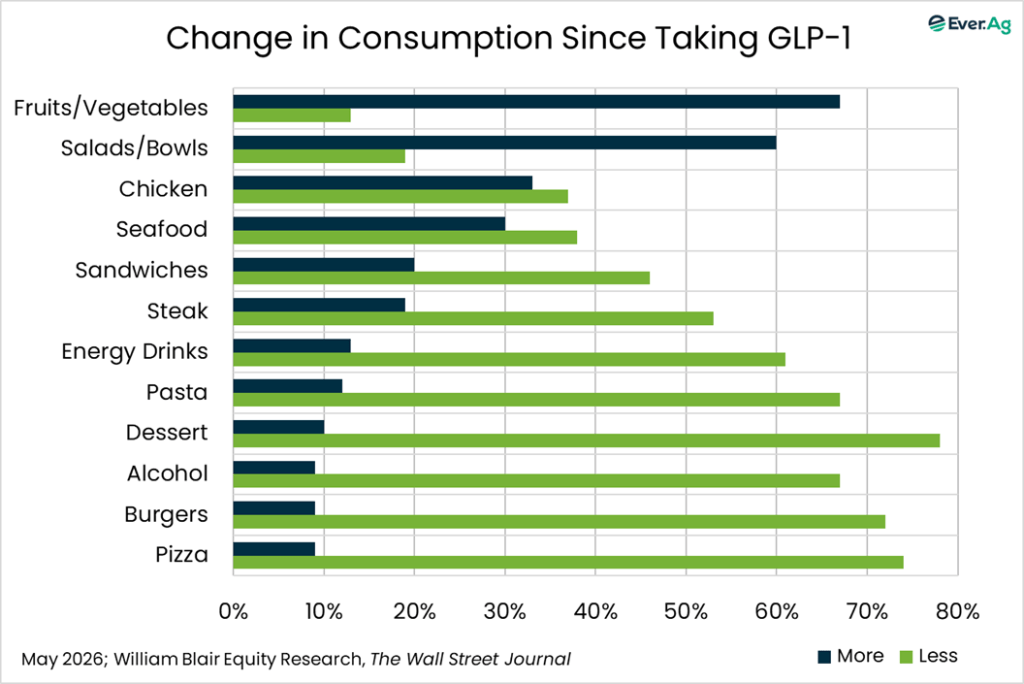

Last week, we learned that… there’s more evidence of GLP-1 users cutting back on burgers and pizza. A survey conducted by William Blair Equity Research found that 72% of GLP-1 users report eating fewer burgers, and 74% report eating less pizza. Only alcohol consumption (78% drinking less) fared worse. Meanwhile, 67% said they are eating more fruits and vegetables. When it comes to meat, 33% say they are eating more chicken, while 37% say they are eating less. For steak, it’s 19% in the more column, with 53% eating less.

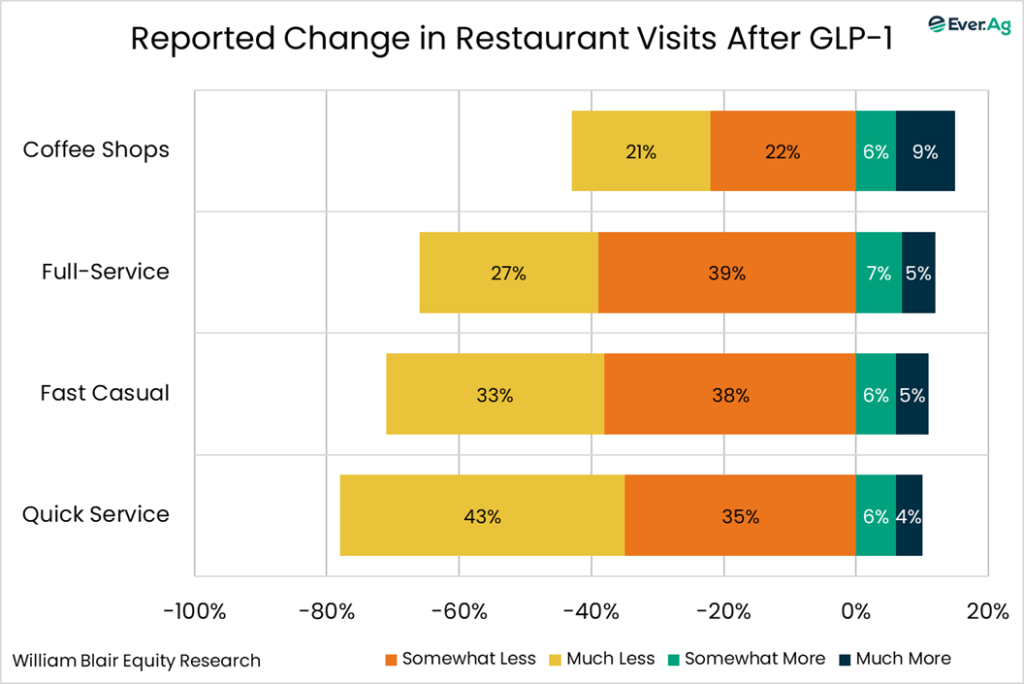

According to the same survey, 43% of GLP-1 users say they are making “much less” visits to quick service restaurants, with 35% indiating “somewhat less” frequency.

A story in The Wall Street Journal spotlighted increasing attention on restaurant performance (emphasis mine):

“We need to have our eyes wide open and adapt,” said Domino’s Pizza CEO Russell Weiner in an interview earlier this year. “Diets are changing.” Kaye Kohlmann, a 45-year-old nurse from Wisconsin, said she ate out four to six times a month before she and her husband started on a GLP-1 treatment in January. Since then, their restaurant visits have declined by half, including fewer trips to McDonald’s and Burger King. “I definitely eat less and make better choices,” said Kohlmann, who works for a company that markets GLP-1s… Wall Street is increasingly pressing company executives about the drugs’ effects on sales… About three months ago, fast-casual chain Panera Bread started surveying customers to understand their GLP-1 usage. The chain found that 17% of customers were taking the drugs, a rate higher than the national average, and they were interested in small portions. “They want healthy, but delicious things that they actually want to eat,” said Jill Marchick, Panera’s vice president of consumer insights. Panera has started offering options geared toward them, including salads stuffed inside Italian bread, and deals for half sandwiches and salads. Olive Garden, famous for its unlimited, buttery breadsticks, started offering a lighter portions menu nationwide this year, partly aimed at GLP-1 users. Chain owner Darden Restaurants has said that the lighter menu is geared to many kinds of consumers, including those looking to spend less money. Customers who order from the menu are increasing their restaurant visits, though the cheaper items are less profitable than full-size portions.

In one way or another, the trend equates to less food demand, limiting upside price potential in several food and agricultural commodity markets.

* * *

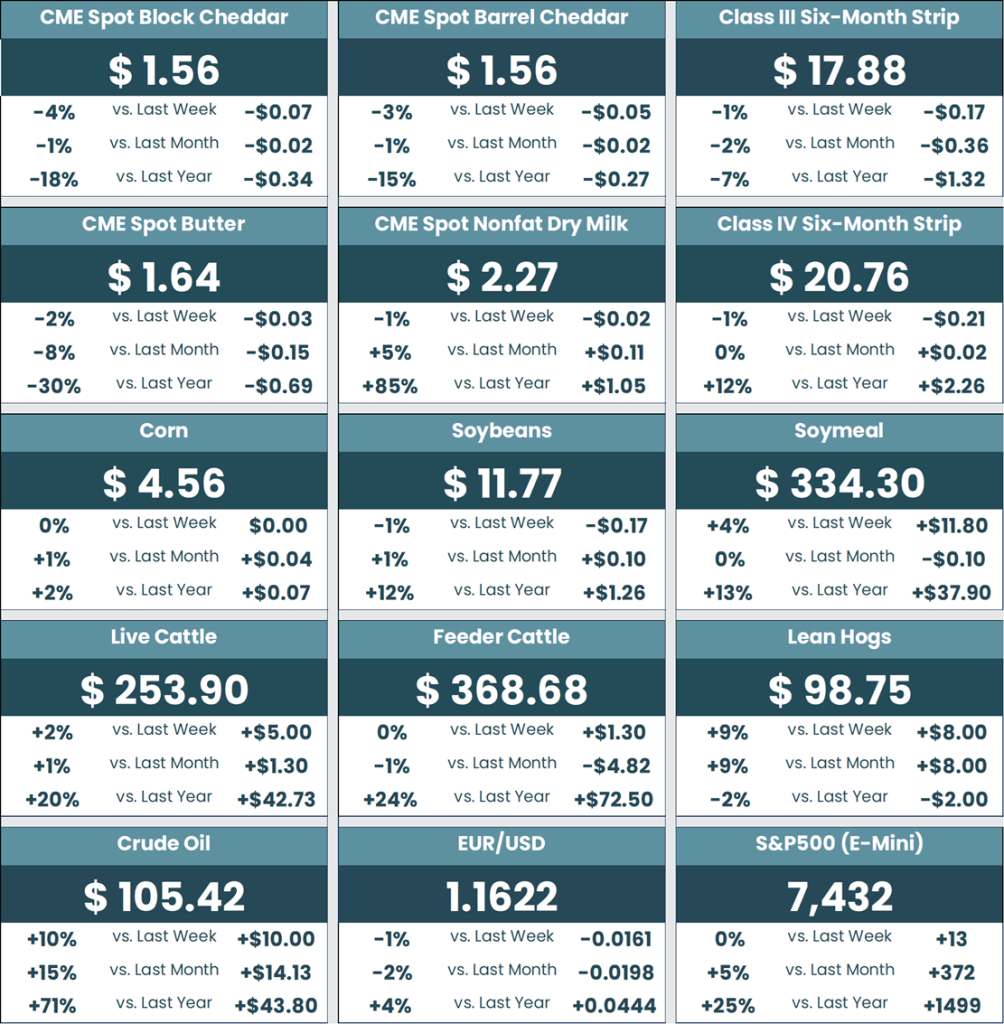

WTI crude oil closed at $105 per barrel on Friday, setting the stage for even higher gasoline prices. As of Saturday, May 16, AAA had the US average price at $4.52 per gallon, down a penny on the week but up $1.33 year-over-year.. Using last week’s DOE/EIA average of $4.50 per gallon, my math shows average weekly household spending on gasoline up $39 year-over-year. If gasoline reaches $5.00 per gallon, the figure jumps to $52 more per week. In my estimation, we’re ratcheting up the pressure on restaurant spending, especially in the QSR space. We still don’t see a collapse in traffic, but Placer.Ai data for the week ending May 10 showed QSR foot traffic down 3.1% year-over-year, making it seven of the last nine weeks in negative territory. Contacts in the cheese and meat trades report that orders from foodservice customers continue to soften, creating some demand headwinds. That’s not likely to change until gasoline prices retreat materially.

* * *

Higher gasoline prices pushed headline inflation and retail sales higher in April, but not to a surprising degree. The Consumer Price Index for all goods and services increased 0.6% on the month and 3.8% compared to April 2025, the biggest year-over-year increase since May 2023. Energy led the way at +3.8% month-over-month and +17.5% year-over-year. Food at home inflation increased by 0.7% from March to April, the biggest month-to-month gain since August 2022, and rose 3.0% versus April 2025, the biggest year-over-year gain since July 2023. You have to wonder whether higher energy prices played a role there, too, since, outside of beef, we haven’t seen much upward movement in food commodity prices. Restaurant prices increased 3.6% year-over-year. The Ever.Ag Breakfast Index came in at $1.93 per serving, down fractionally on the month and down 20% year-over-year, mostly because egg prices are sharply lower.

Gasoline stations obviously took in a lot more money in April, with the US Department of Commerce Retail Sales report putting the total at $61.5 billion on a seasonally adjusted basis, up 20.8% year-over-year. That propelled overall retail sales to a 4.9% year-over-year advance.

Sales growth at food outlets trailed inflation, with the food service take up 2.7% year-over-year (inflation +3.6%) and grocery stores at +1.6% versus April 2025 (inflation +3.0%). So, for the fifth month in a row, our measure of combined, inflation-adjusted restaurant and grocery sales declined year-over-year, this time by 1.0%. This trend continues to lend support to our notion that, collectively, Americans are buying less food than they did a year ago.

* * *

We still haven’t given up on beef, however. According to Circana data compiled by Anne-Marie Roerink at 210 Analytics, retail beef sales volume increased 1.6% year-over-year, bringing the winning streak to 22 months. This despite retail ground beef prices reaching a new record high of $6.90 per pound (up 3.0% on the month and up 18.7% year-over-year).

* * *

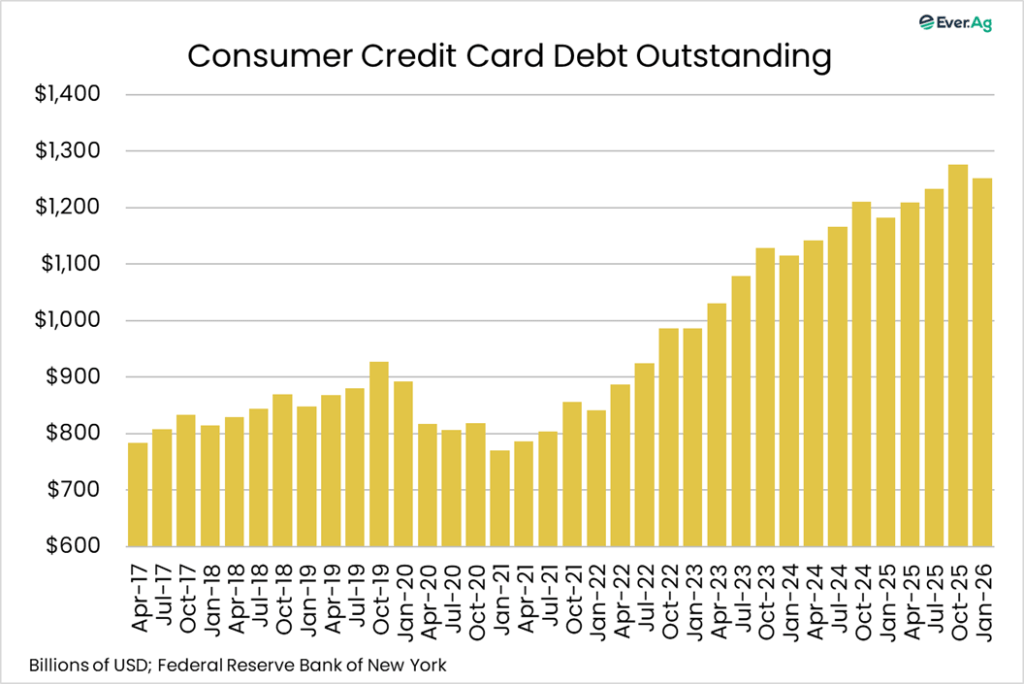

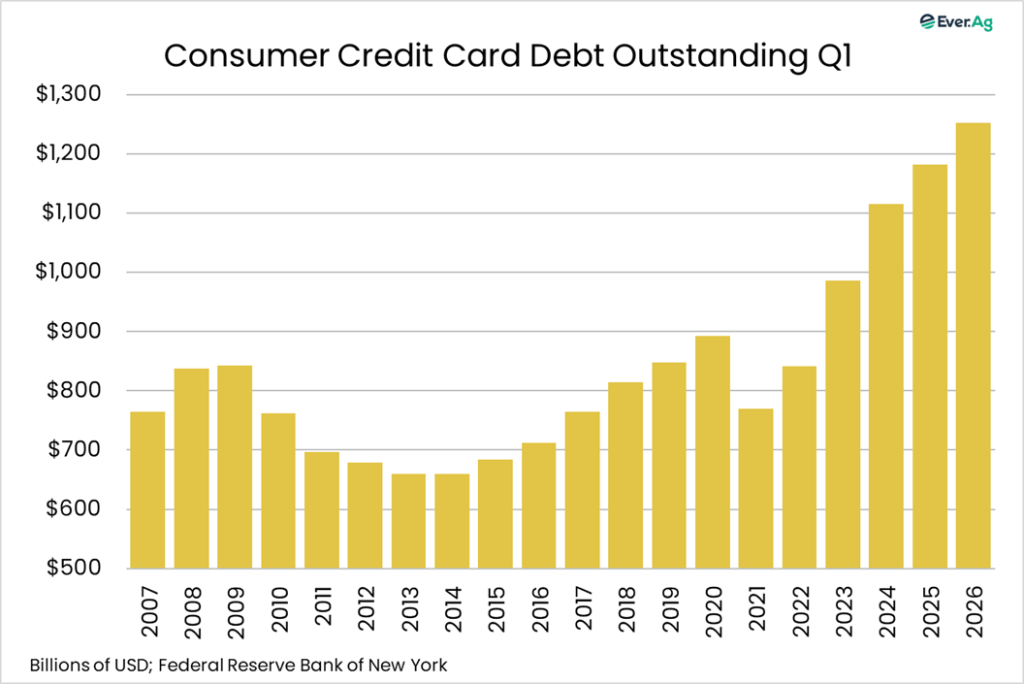

Don’t let the retreat in Q1 credit card balances fool you; consumers are more in debt than they were a year ago. According to the latest data from the Federal Reserve Bank of New York, credit card balances totaled $1.252 trillion, down 2.0% compared to Q4 2025. Before getting too excited about balances moving backward quarter-to-quarter, it’s worth noting that balances almost always decline in Q1, presumably as consumers pay off some of the debt incurred during the holiday season. In fact, this year’s pullback was slightly below the 10-year average (-2.5%). Delinquency data had a mixed look, with 8.6% of accounts termed newly delinquent (30 days), down from 8.7% the prior quarter. Meanwhile, the percentage of accounts becoming seriously delinquent reached 13.1%, up from 12.7% in Q4 2025 to the highest level since Q4 2010.

I continue to see the credit card situation as tenuous, but not yet disastrous, not least because income continues to rise and the employment situation remains decent. But with gasoline costs up, it wouldn’t be a surprise to see bigger upticks in credit card debt in the months ahead as consumers attempt to cope with higher prices.

* * *

Butter sales remain solid, as post-Easter promotions drive business. For the week ending May 10, Circana reported volume up nearly 4% year-over-year. Price averaged $4.45 per pound, down two cents on the week and down 11% year-over-year. Natural cheese sales increased fractionally, with the average price at $4.90 per pound, down four cents on the week and down 4% year-over-year.

Futures and options on futures trading involves significant risk and are not suitable for every investor. Information contained herein is intended for informational purposes and is obtained from sources believed reliable but is in no way guaranteed. Past results are not indicative of future results. Any data contained herein is proprietary and may not be copied, disseminated, or used without the express written permission of Ever.Ag Insights.