The Scoreboard

Comment

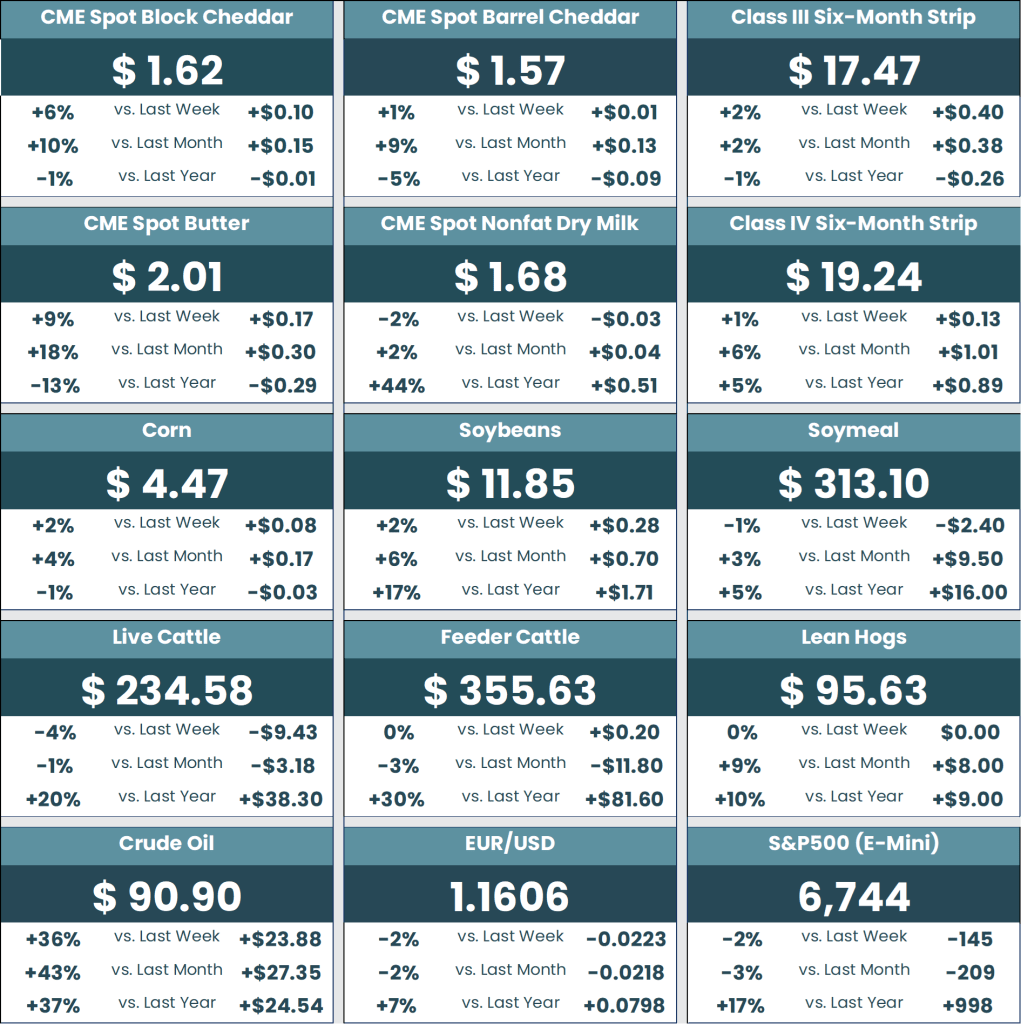

Last week, we learned that… A spike in gasoline prices now belongs at the top of the US economic worry list. Military action in Iran pushed WTI crude to $90.90 per barrel, up 36% for the week — the highest Friday close since October 2022 and the largest week‑to‑week gain since WTI began trading on NYMEX in 1983. Gasoline prices are rushing higher as a result, with AAA reporting the national average for unleaded at $3.45 per gallon on Sunday, up from $2.98 a week earlier and $2.90 a month ago. The last time we saw WTI this high, regular unleaded prices averaged about $3.80 per gallon.

If we get there again, an 80‑cent per gallon move from mid‑February, the hit to consumers adds up. Based on DOE “product supplied” data, the US burns about 3.31 billion gallons of gasoline per week. An 80‑cent increase translates to roughly $2.65 billion in additional weekly fuel costs. Spread across the 120 million US households that own a car, that’s about $22 per week per family. That’s not a disaster, but where does the money come from? We always worry that “restaurant spending” may be the answer for some. Whether it shows up in QSR traffic or other discretionary spending categories, higher gasoline prices reverse what had been a clear win for consumers. That reversal matters. In a recent Washington Post/ABC News poll, 71% of Americans said gasoline was affordable, even as 53% reported they are “just hanging on” financially. That cushion is gone, at least for now. And risks remain.

A crude oil move toward the $120 level seen in 2022 would reopen the door to $5.00‑per‑gallon gasoline. Overnight, crude traded over $100 per barrel, so the watch is on.

Can the White House turn to the Strategic Petroleum Reserve for relief? Last week, in an interview with Reuters, President Trump said that it wasn’t likely:

“I don’t have any concern about it,” he said, when asked about the higher prices at the pump. “They’ll drop very rapidly when this is over, and if they rise, they rise, but this is far more important than having gasoline prices go up a little bit.”

Even if he had the appetite, the SPR isn’t what it was before the Biden Administration tapped the stockpile to address the 2022 crude oil rally. During the last week of February, SPR stocks totaled 415.4 million barrels, up 5% year-over-year, but down 35% from the same week in 2021.

* * *

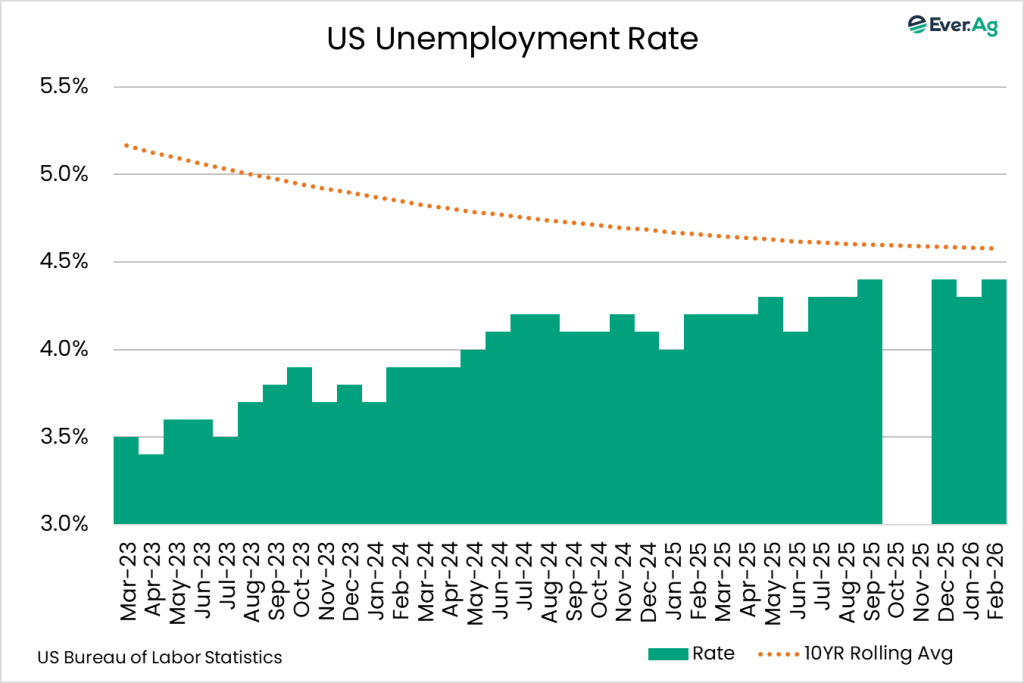

I found one figure in the latest Employment Situation report especially troubling. According to the US Bureau of Labor Statistics, the mean duration of unemployment reached 25.7 months in February, a two-month jump from January to the highest level since January 2022. It’s taking people longer to find new jobs once they lose or leave their previous position, a dynamic that tends to weigh on confidence and discretionary spending. That’s the sense you get from reading various stories and listening to various shows; this data point puts a number to it. Headline employment data wasn’t encouraging either, with payrolls down 92,000 positions (analysts expected +60,000) and the unemployment rate rising to 4.4%.

Last week’s labor news wasn’t all ugly. The Challenger, Gray & Christmas Job Cuts report showed fewer terminations in February, with 43,307 positions eliminated, down from January’s aggressive total of 108,435 and 172,017 in February 2025.

As noted in recent months, I expect labor conditions to hang on in much the same fashion as the overall economy. It’s been the same story for several months now: some bright spots, some troublesome ones, and not much change in the overall trajectory.

* * *

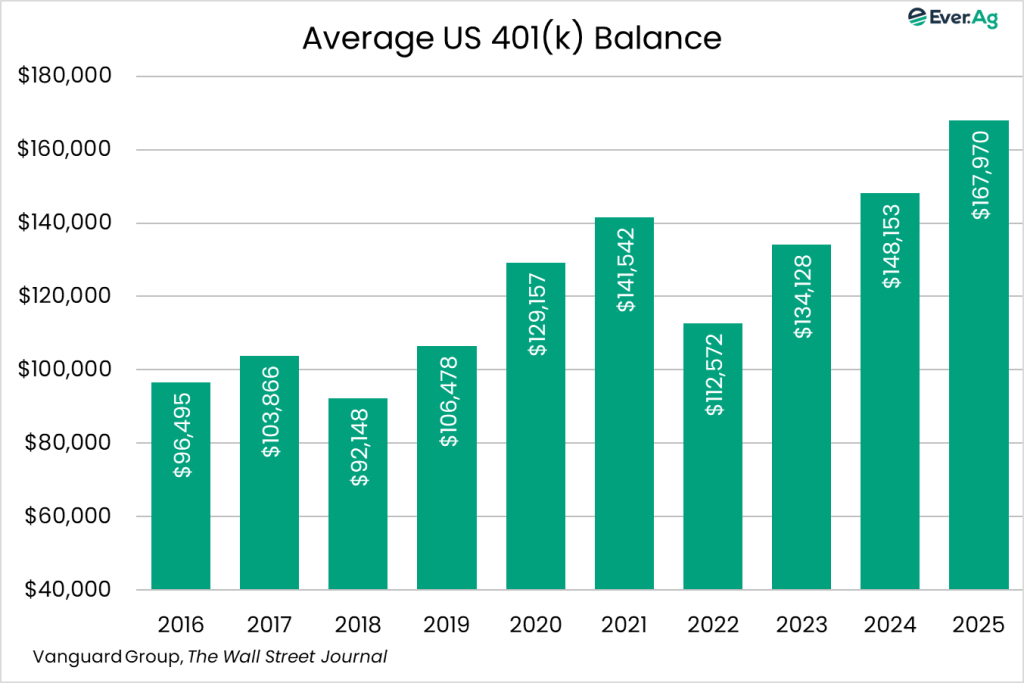

The headline in The Wall Street Journal was an attention-grabber: “Record Number of Workers Are Raiding Their 401(k) Savings.” According to Vanguard, a record 6% of working plan participants took hardship withdrawal, up from 4.8% in 2024, offering another illustration of strain in segments of the economy. According to the story:

The uptick in hardship withdrawals marks the sixth straight year of increases since 2018, when Congress made it easier to take a hardship distribution by eliminating the requirement to take a 401(k) loan first, according to Vanguard, which administers 401(k)-type accounts for nearly five million people. The top reasons for taking hardship withdrawals last year were avoiding foreclosure and eviction, and paying medical expenses, according to Vanguard. The median withdrawal was $1,900. In recent years, Congress has also expanded the list of allowable reasons to take a hardship withdrawal. Under a 2022 law, it gave employers flexibility to permit them for victims of domestic abuse and federally declared disasters. That law also lets people take out up to $1,000 penalty-free for an emergency once every three years. Those who replace what they take out can tap their accounts again the next year. Another factor behind the rise is the spread of automatic enrollment. As it has moved more workers into 401(k) accounts, it is giving more people savings to draw on. (Workers can opt out of automatic enrollment, but many fail to take that step.)

The good news in the story? Stock market gains also continue to push average account values higher. Vanguard reported an average account balance of $167,970, up 13% from 2024 and 74% from 2015.

* * *

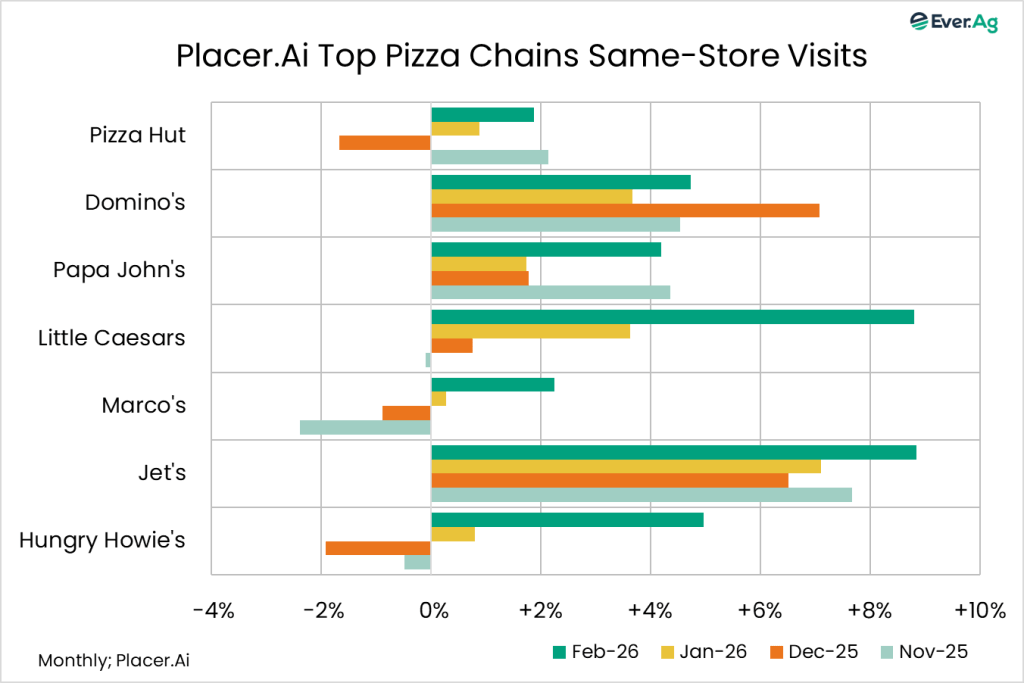

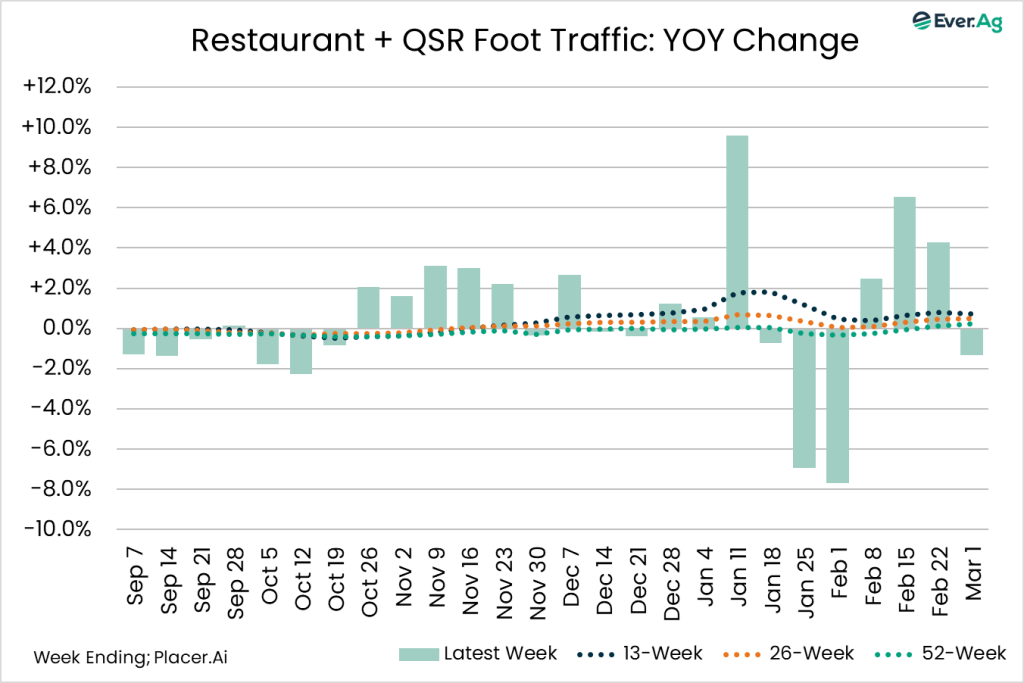

Restaurants and QSR outlets enjoyed a sneaky good February — can it last? Data from Placer.Ai showed food traffic up 3.2% year-over-year, the best performance since February 2024.

Looking at same-store visits for large pizza chains, all seven we follow posted results for the second month in a row, and each showed improved performance from January. My sense: “Big pizza” seems to be promoting more aggressively in early 2026, looking to shake off middling Q4 sales and, perhaps, leaning into lower cheese costs. I asked Microsoft CoPilot for its assessment of Little Caesars activity because, to my eye, that chain seemed to pump up the volume on deals and enjoyed outsized traffic growth. Here’s what CoPilot said:

Compared with Q4, YTD promotional activity has been more price‑led and less driven by the promotional calendar. The emphasis has shifted from “lots of deals” to “one very loud deal”, reinforcing the idea that value competition intensified meaningfully as 2026 got underway.

“Big burger” performance wasn’t as uniform, with four of the eight chains we follow in positive territory and four experiencing traffic declines. But that was better than in January and last February.

Starbucks — another chain we follow from a dairy perspective, especially since protein lattes debuted in October — enjoyed a big February, with same-store traffic up 9% year-over-year, the biggest jump since January 2023.

This all seems positive from a dairy and beef demand perspective. I wonder, however, if consumers simply got out more in February because massive weather events such as mega-storm Fern kept people away from restaurants in January. And, now, we also have to worry about higher gasoline prices chipping away at discretionary spending as long as the military conflict in the Middle East persists. Activity didn’t look as robust during the week ending March 1. We’ll monitor what happens from there.

* * *

Butter, cheese, and milk sales all landed in positive territory during the week ending March 1. According to Circana, butter & butter blend volume sales increased by nearly 2% year-over-year, bringing the winning streak to six weeks. Price averaged $4.59 per pound, down 15 cents on the week and down 8% year-over-year. Natural cheese sales increased by 1% to 2%, the best showing since Storm Fern rolled through in late January. Average price: $4.90 per pound, unchanged on the week and down 4% year-over-year. Fluid milk sales increased by about 1%.

* * *

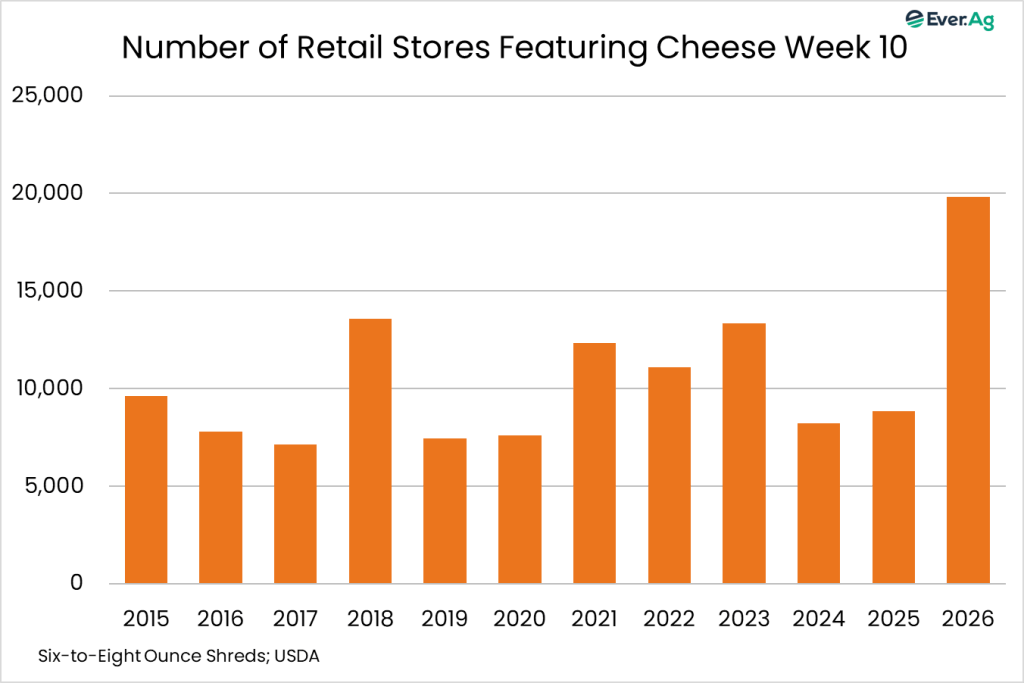

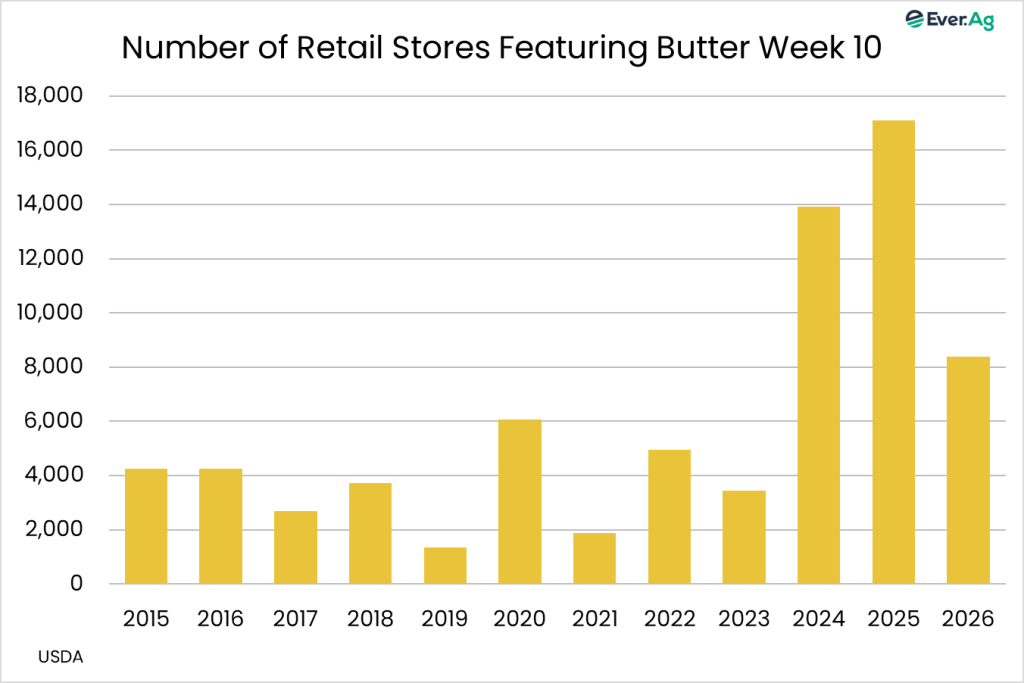

Cheese promotions take center stage this week while butter activity fades. USDA reports 19,836 stores running deals on six-to-eight-ounce shreds this week, up 90% on the week and up 124% year-over-year to the highest level since November 2023. We’re also seeing aggressive pricing: $2.24 per package, down 41 cents for the week and 3% year-over-year. Butter activity slips to 8,391 stores, down 30% from the week prior and down 51% year-over-year. Average price: $3.54, up a penny on the week and down 29% year-over-year.

Futures and options on futures trading involves significant risk and are not suitable for every investor. Information contained herein is intended for informational purposes and is obtained from sources believed reliable but is in no way guaranteed. Past results are not indicative of future results. Any data contained herein is proprietary and may not be copied, disseminated, or used without the express written permission of Ever.Ag Insights.