The Scoreboard

Comment

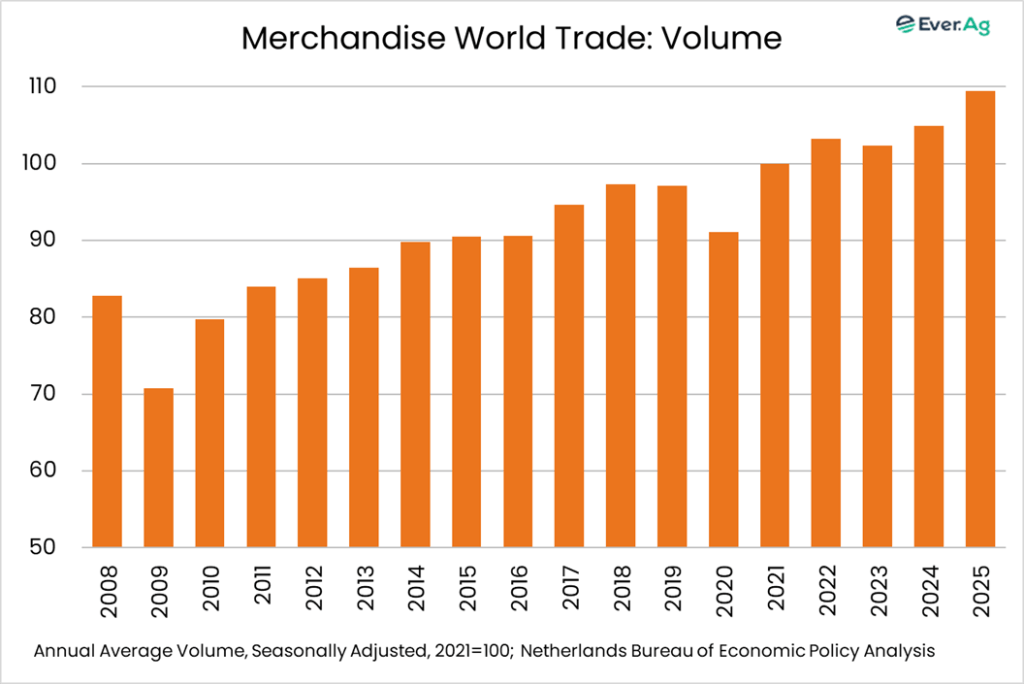

Last week, we learned that… a measure of world trade suggests that the world economy might be in better shape than we thought. For all the worries about tariffs and concerns about global economic growth, cross-border trade in goods increased by 4.4% in 2025, according to the Netherlands Bureau for Economic Policy Analysis (also referred to as CPB).

Zooming in, both developed and emerging economies enjoyed better activity, with growth in imports at +4.1% and +4.3%, respectively. While conditions in China remained soft (imports grew by only 0.2%), other emerging economies in Asia saw inbound goods traffic surge by 10.4%. That may reflect recovery from punishing inflation from 2021 to 2023 and a weaker USD. Latin America also saw a significant increase in imports, up 7.1% year-over-year. CPB notes that recent months show a volatile pattern likely tied to tariff announcements and subsequent delays/adjustments — suggesting some timing effects — but the breadth of improvement still points to more resilience than many expected.

One important nuance: CPB flagged that recent trade data can look choppy because tariff announcements (and subsequent delays/changes) can pull shipments forward and then leave a hole later. Still, the breadth of the 2025 gains is a constructive signal. If it persists, it’s another reason to be at least modestly more bullish of dairy and other ag commodities including pork.

* * *

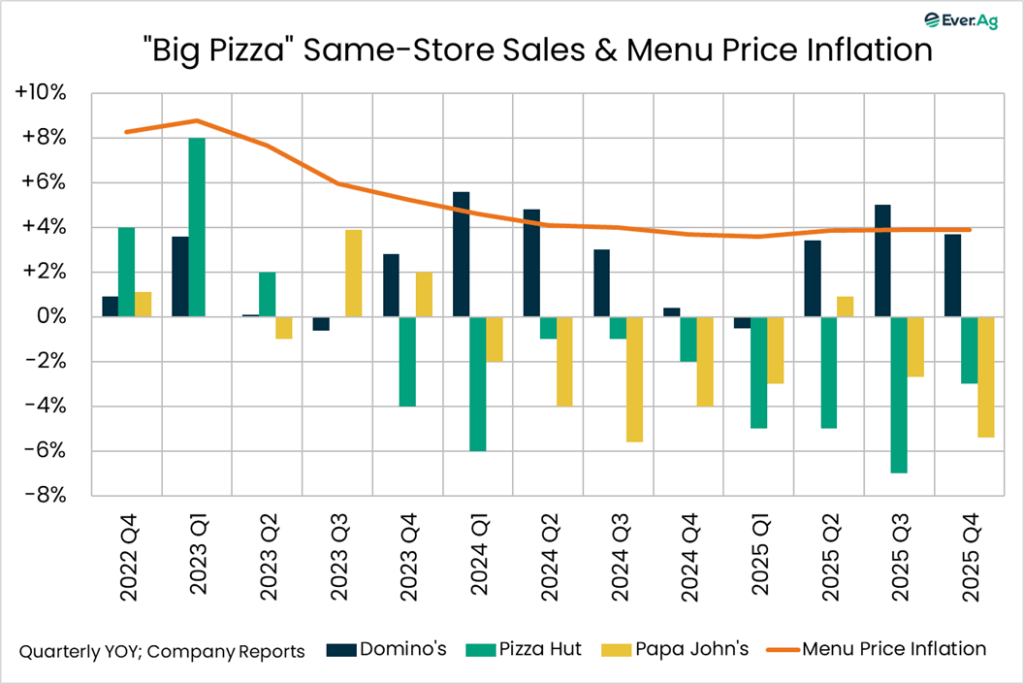

“Big pizza” endured another mediocre quarter, and now we’re seeing the fallout. Last week, Papa John’s reported that US same-store sales declined 5.4% in the fourth quarter, the worst showing since 2019. The company announced that it would close 300 underperforming units over the next year. Earlier in February, Pizza Hut said same-store sales declined 3.0% and told Wall Street it would shutter 250 stores. That’s a lot of closures — about 5% of the combined total for the companies. Consumers are eating less pizza. Papa John’s CEO Todd Penegor noted that his company was seeing a lot of size trade downs into medium, providing “a little bit of pressure on our business…”

Domino’s fared better, with same-store sales up by 3.7%, but even that trailed the rate of food-away-from-home inflation for the quarter.

Less pizza consumption means less cheese and pepperoni consumption, potentially eroding demand for suppliers.

* * *

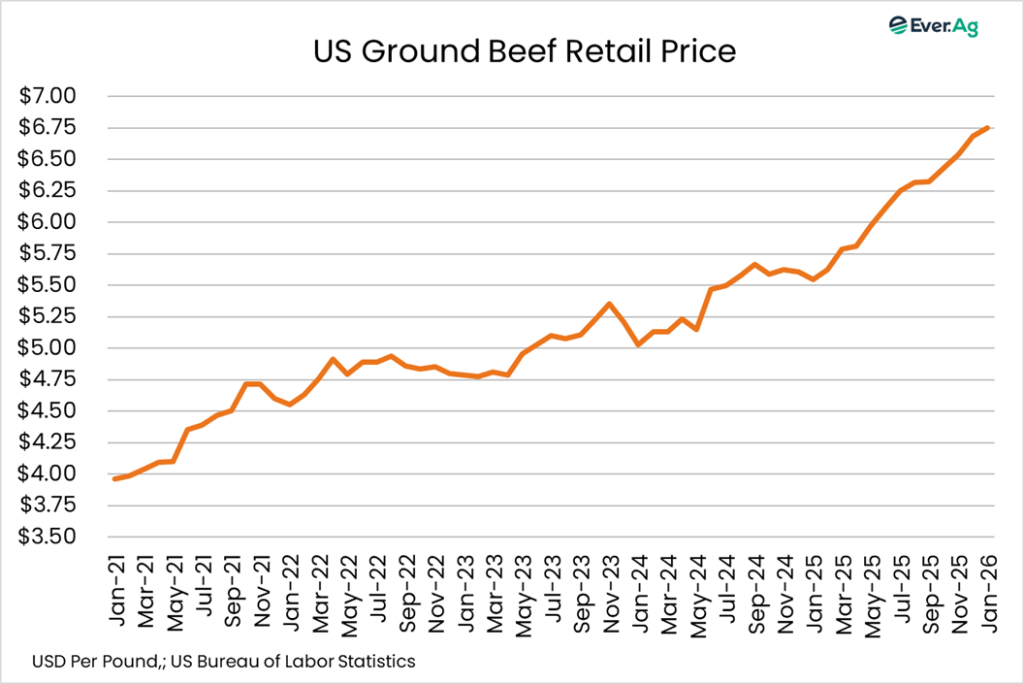

Americans continued to buy more beef in January, with the mega-storm Fern likely adding to the push. Circana data compiled by Anne-Marie Roernik of 210 Analytics and published by National Provisioner showed fresh beef retail volume up 4.7% year-over-year, the best showing since May. This happened even with ground beef prices reaching a new all-time high of $6.75 per pound nationally (up 22% year-over-year). Elsewhere, pork sales volume increased 2.9%, with chicken up 2.6% and bacon down 1.0%. The scramble to stock up ahead of Fern’s arrival made a difference, though. According to Roernik:

In the first, second, third and fifth weeks of January, pound sales were down year-on-year for the total meat department as well as the two biggest sellers, beef and chicken. The arctic storm that impacted many states led to sold-out meat cases and a 31% surge in dollar sales the week ending January 25. Volume rose by more than 25%, with beef volume climbing even higher, at +30.3% over the same week in 2025.

Continued beef demand strength at high prices increases the odds that dairy farmers will continue to see solid income from their day-old calf sales.

* * *

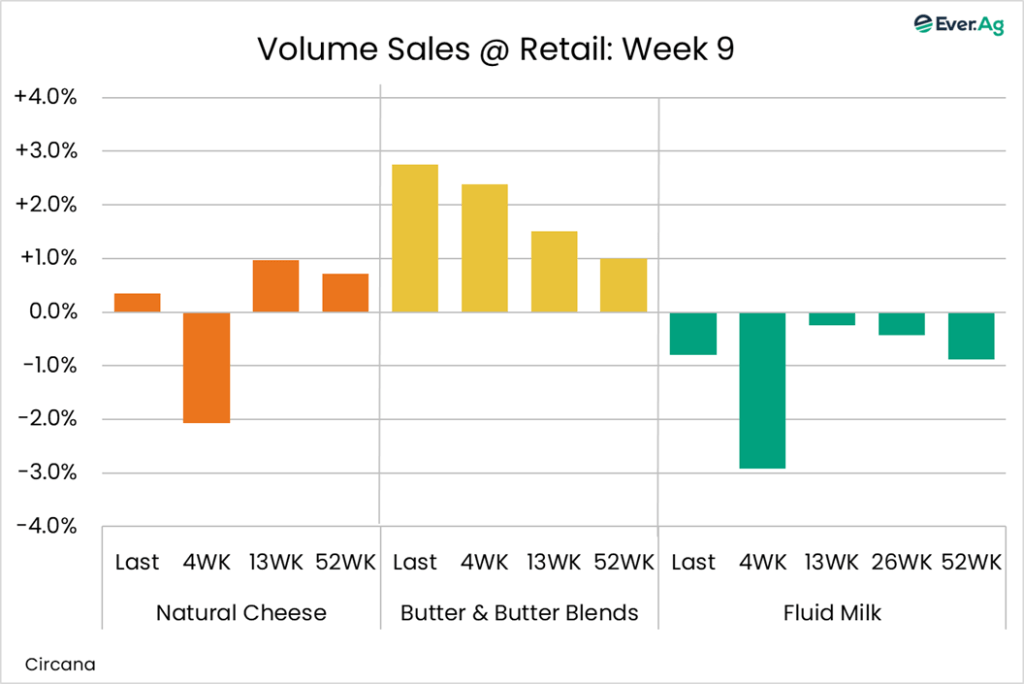

Butter sales stayed strong during the first week of Lent. According to Circana, butter & butter blend volume sales increased by nearly 3% year-over-year during the week ending February 22, marking the fifth consecutive week with positive results. The average price increased to $4.74 per pound, up eight cents on the week, but down 9% year-over-year. Natural cheese sales got back into the black, but barely, with volume up fractionally. Average price: $4.90 per pound, down two cents on the week and down 4% year-over-year.

* * *

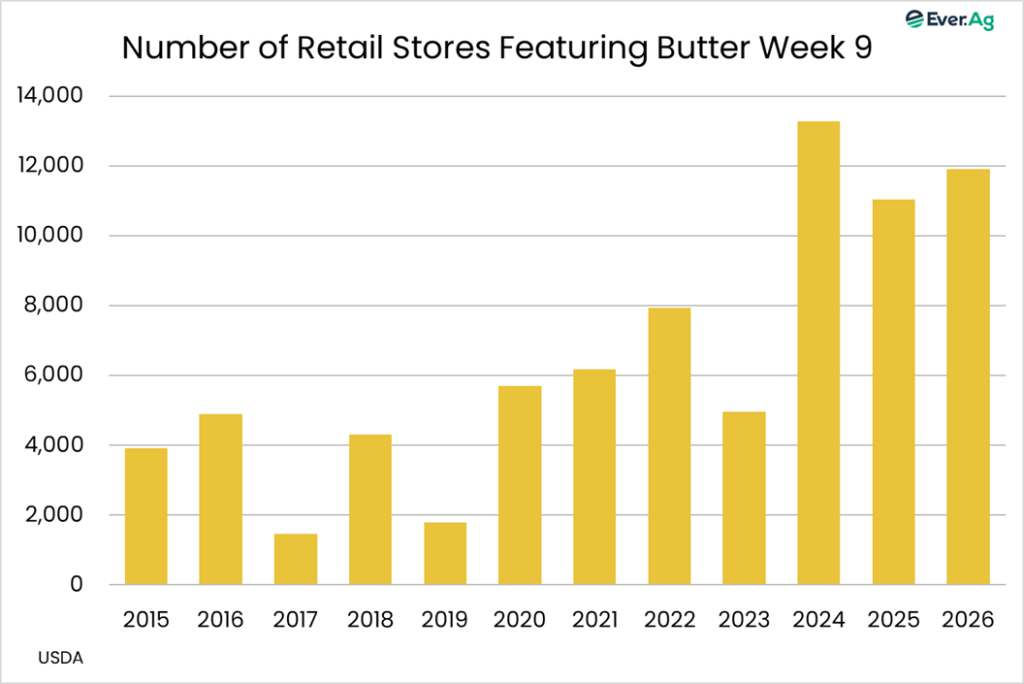

More promotions and lower prices should keep butter sales rolling. USDA reports that 11,920 stores have butter deals for the week ahead, up 36% from the week before and 8% year-over-year. The average price drops to $3.53 per pound, down three cents on the week and down 24% year-over-year. Things remain less active for cheese, with 10,455 stores featuring six-to-eight-ounce shreds, down 12% from the prior week and 5% year-over-year. Average price: $2.65 per package, up 49 cents on the week and up 15% year-over-year.

Futures and options on futures trading involves significant risk and are not suitable for every investor. Information contained herein is intended for informational purposes and is obtained from sources believed reliable but is in no way guaranteed. Past results are not indicative of future results. Any data contained herein is proprietary and may not be copied, disseminated, or used without the express written permission of Ever.Ag Insights.