The Scoreboard

Comment

Last week we learned that… Walmart continues to win, in part by gaining share with upper-income households. Walmart’s same-store sales continued to grow in Q4, with the company reporting a 4.6% increase, identical to Q3 and year-prior levels. Analysts expected to see +4.3%. CFO According to CNBC:

In an interview with CNBC, CFO John David Rainey said speedy deliveries from stores are helping Walmart attract more shoppers, particularly those with higher incomes. “Our ability to serve customers at the scale that we have, combined with the speed that we now have, is really translating into continued market share gains,” he said. Rainey said the company’s market share gains cut across all incomes, but were larger among upper-income households. For example, with fashion, a category that grew by a mid-single-digit percentage in the fourth quarter, almost all of that increase came from households with an annual income over $100,000, he said… While Walmart is gaining ground, its growth is not evenly distributed across income groups. In the interview with CNBC, Rainey said the company does “see some pressure on the lowest income cohort.” He said Walmart has tracked year-over-year spending trends by income group. Like in the prior quarter, he said it saw that spending among the highest earners compared to lower-income groups “had gapped out a little bit.”

Looking at Placer.Ai traffic data, consumers continued to choose Walmart in January, with same-store visits up 3.8% year-over-year, beating Target (-0.1%), Albertsons (+1.2%), and Safeway (+0.7%). Foot traffic at Dollar General, an even deeper discounter, gained +4.9%, while Kroger (somewhat incongruously) ran at +4.0%.

The message in all of this: consumers continue to look for value, even as headline inflation cools.

* * *

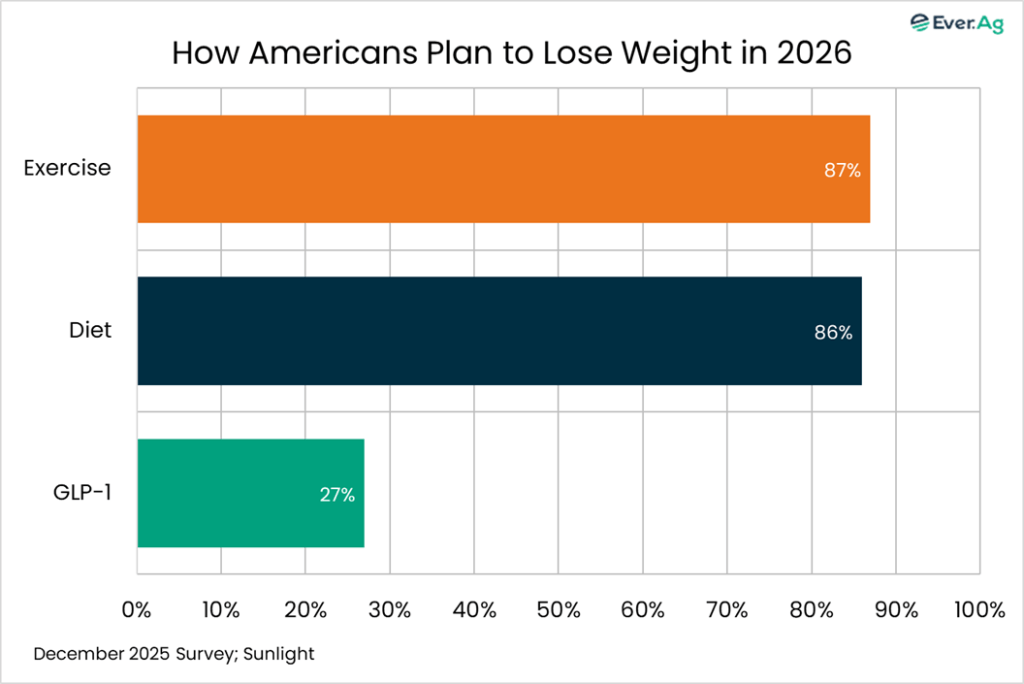

Adapt or suffer the consequences. Just about every week, I stumble across an article or two showing new data about GLP-1 adoption. This week, for example, I saw survey results from Sunlight, a company that markets weight-loss medications. According to a poll commissioned by Sunlight, 52% of Americans say they want to lose weight in 2026, and 27% (about one in seven) say they anticipate using GLP-1 medications to help along the way. While that’s not surprising, it lends credibility to expectations for continued growth in GLP-1 use.

Consumer packaged goods companies continue to get religion about the risks to their business posed by the ascent of GLP-1 medications, with many altering portion sizes and taking other measures to adapt. A recent story from Reuters offered details:

So far this year, nearly three dozen companies outside the healthcare industry have mentioned GLP-1 drugs or weight loss on their earnings conference calls, up from 14 for the same period a year ago, and just five two years earlier, according to LSEG data. Diet changes linked to GLP-1 drug use could mean up to $12 billion in snack sales lost over the next decade, according to EY-Parthenon estimates… Peter ter Kulve, CEO of Magnum Ice Cream, said GLP-1 users continue to eat treats, but they exhibit “a stark reduction of mindless munching and binge eating.” PepsiCo has launched a line called “Simply NKD” to reformulate its snacks, and is rebranding products such as Lay’s and Gatorade by removing artificial colors. PepsiCo will also begin testing mini-meal options with its Sabra and Siete brands in the USA, CEO Ramon Laguarta said at the Consumer Analyst Group of New York (CAGNY) conference on Wednesday. “I think there are more opportunities than threats, but there are both,” Laguarta said on a post-earnings call earlier this month. Coca-Cola ramped up production to meet growing demand for its protein-infused Fairlife milk late last year. General Mills launched higher protein Cheerios cereal in December 2024 as it grapples with competition for breakfast foods. “We expect GLP-1 and other anti-obesity drugs to have a lasting influence in the food and nutrition landscape, nudging some consumers towards smaller portions and more nutrient-dense protein and fiber-forward foods,” General Mills’ CEO Jeffrey Harmening said at the CAGNY conference on Tuesday… “We’re just starting to scratch the surface on the ripple effects of this type of physiological disruption,” said Ali Furman, PwC U.S. consumer markets leader.

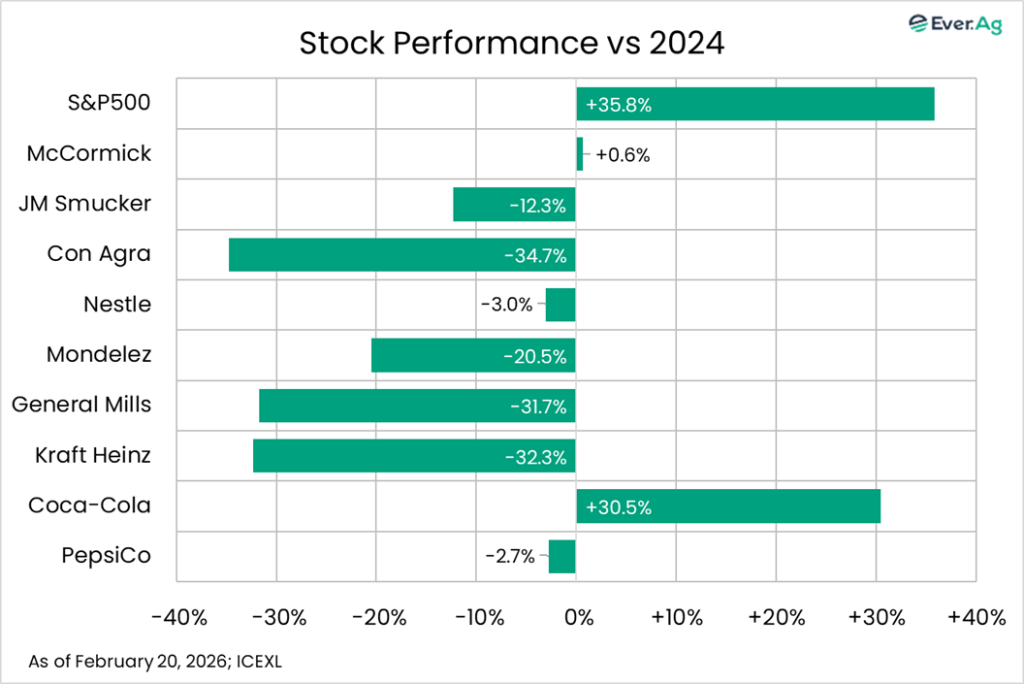

It’s been rough going for many CPG stocks, which are down from 2024 levels during a period when the S&P 500 gained nearly 36%.

Based on what we’re already seeing, it’s probably a safe bet to assume that protein could figure prominently as companies retool their lineups. Is it a coincidence that Coca-Cola, which got on the protein train early with Fairlife and Core Power, is outperforming its peers? Probably not.

* * *

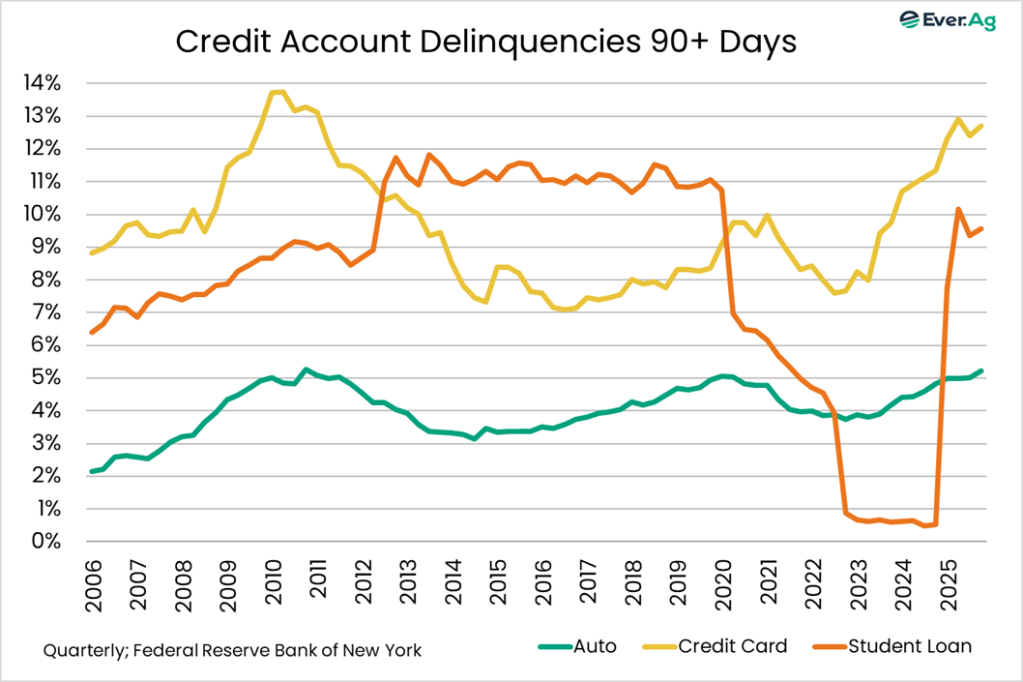

Consumers leaned on their credit cards for year-end holiday spending. The Federal Reserve Bank of New York reported outstanding credit card debt at a record $1.28 trillion, up 3.6% from Q3 and up 5.5% year-over-year. While we’ve seen year-over-year growth decline (it averaged +13.0% from 2022 through 2024), consumers continue to add to the pile. But we are managing to make payments on time, with new delinquencies at 8.7%, down from 8.9% in Q3 and 9.0% a year earlier. The percentage of accounts seriously delinquent (90+ days) did increase to 12.7%, up from 12.4% in Q3 and 11.4% in Q4 2025. That’s almost as high as in 2010 (13.7%).

On other fronts, auto loan balances weren’t much higher than a year ago — $1.67 trillion, up 0.7%. The percentage of newly delinquent accounts edged lower to 7.7%, down from 7.8% in Q3 and 8.1% a year earlier. Student loans are an issue, with the government collecting again, and attaching delinquent status to non-performing accounts.

Are we heading for disaster here? I’m still leaning toward the “no” camp, but these updated figures are trending in a more dangerous direction, leaving me feeling edgier. I maintain that things would move from “concerning” to “alarming” if labor markets deteriorate materially.

* * *

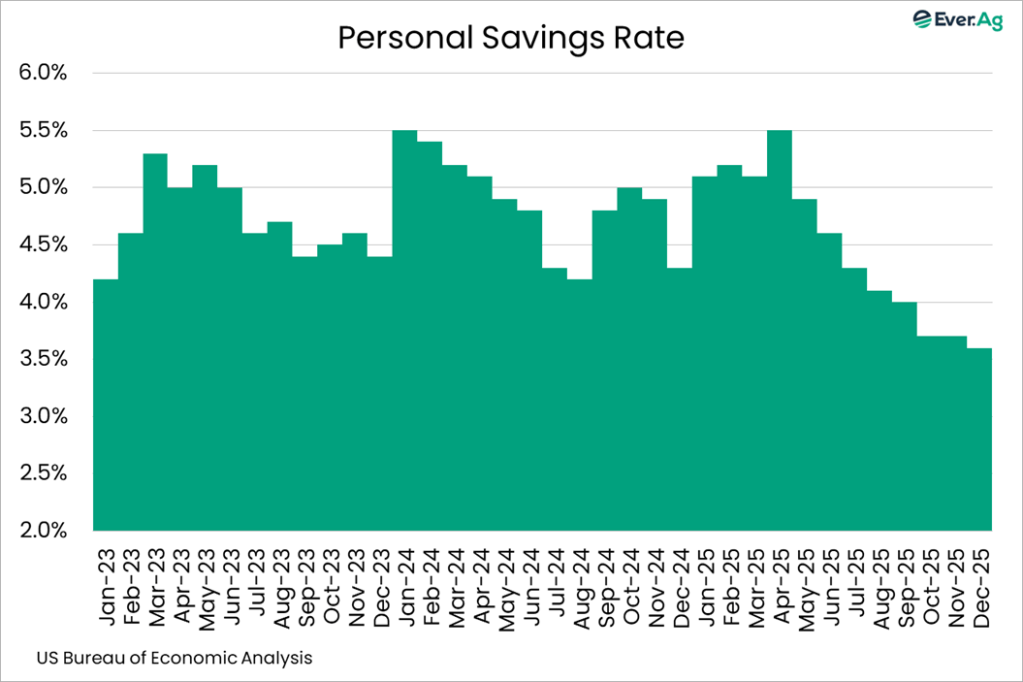

Some consumers may also be increasing credit card use to stay ahead of the monthly squeeze between income and expenses. The personal savings rate published by the US Bureau of Economic Analysis measures the gap between monthly income and monthly expenses. In December, the savings rate came in at 3.6%, down from 3.7% in November and 4.3% a year earlier, to the lowest level for the month since 2007.

* * *

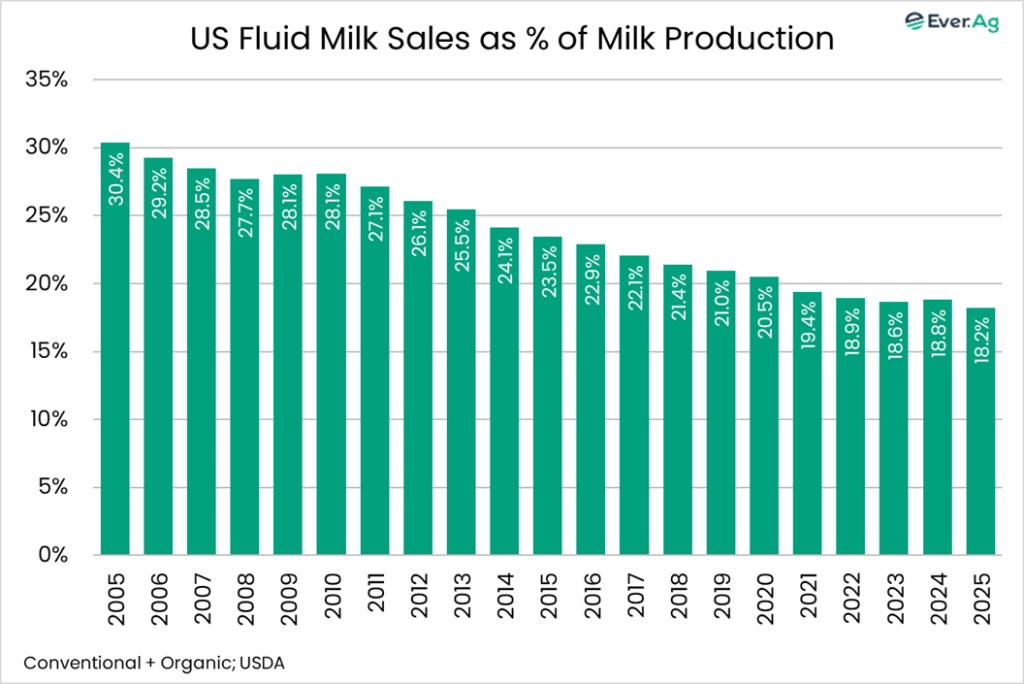

Fluid milk sales ended 2025 on an uptick, but not by enough to push annual volume into the black. According to USDA data, conventional + organic volume totaled 3.763 billion pounds, up 1.2% year-over-year. That put annual volume at 42.213 billion pounds, down 0.6%. Sales equaled 18.2% of reported US milk production, down from 18.8% in 2024 and 30.5% in 2005. Whole milk continued to gain share, accounting for 37% of sales. Softer fluid sales mean more milk available for other purchases. For all of 2025, fluid volume fell 260 million pounds short of the 2024 total, enough milk to make about 11 truckloads of cheese per week.

* * *

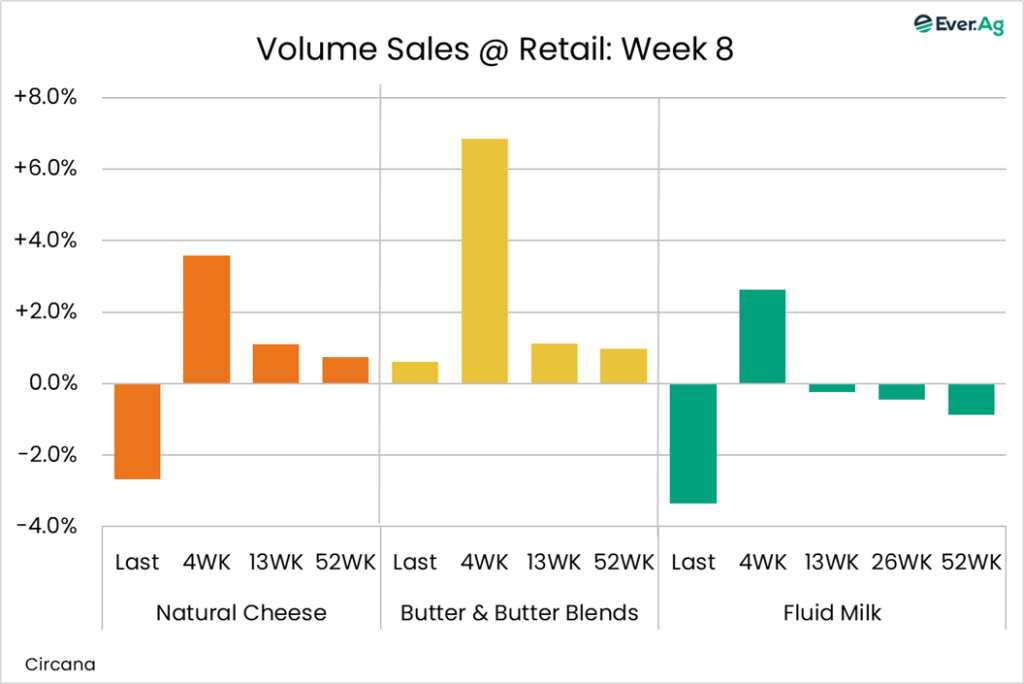

Butter sales stay in positive territory; natural cheese sales remain negative. According to Circana, for the week ending February 15, butter & butter blend sales increased by about 1%, the smallest gain in four weeks, but a gain just the same. Prices averaged $4.66 per pound, up seven cents on the week but down 9% year-over-year. Natural cheese volume sales declined by nearly 3%. Retail price averaged $4.92 per pound, up five cents on the week and down 3% year-over-year. Fluid milk sales declined by more than 3% when compared to the same week a year ago.

* * *

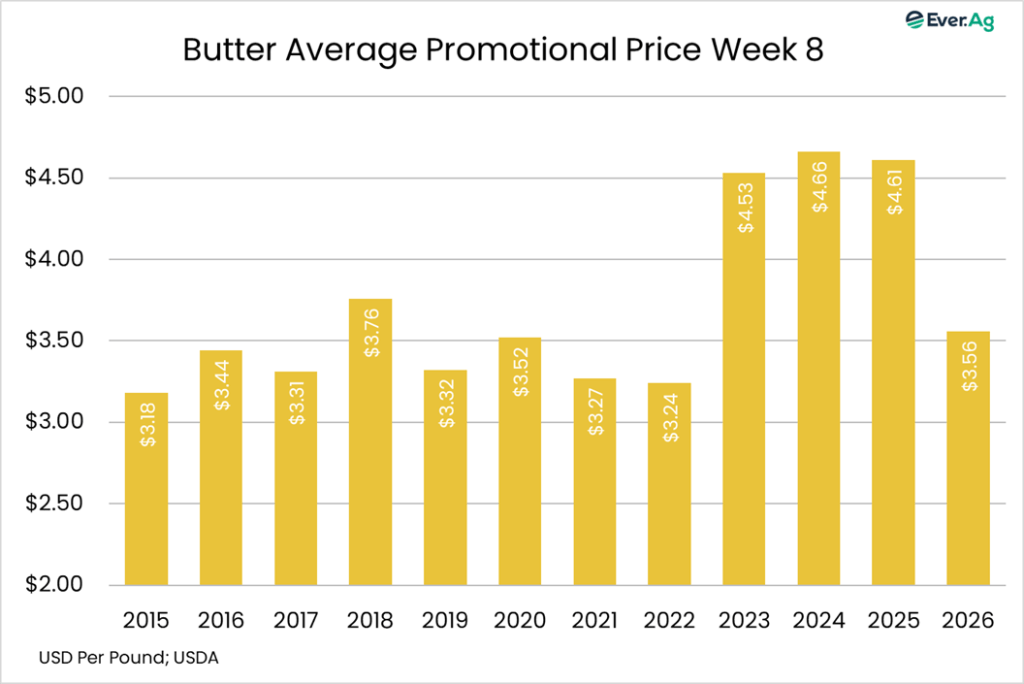

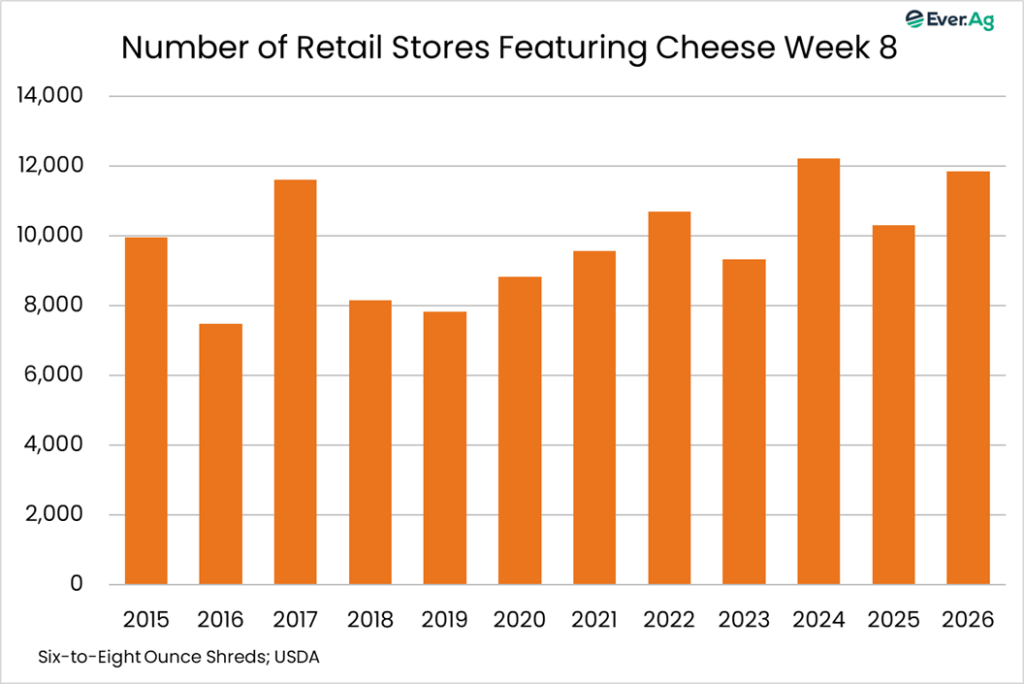

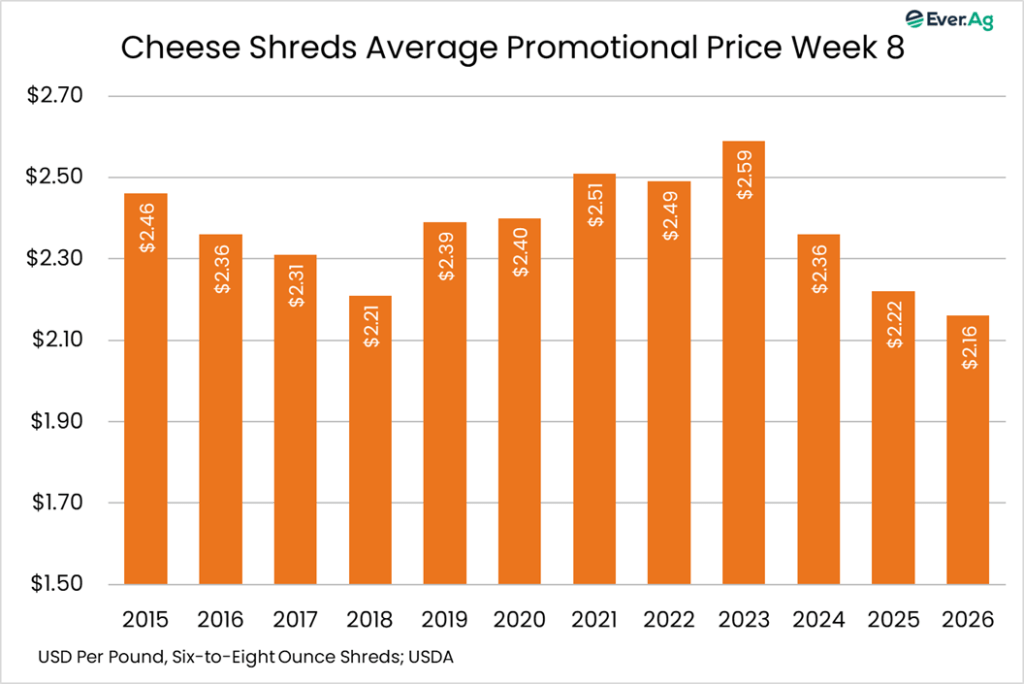

Butter and cheese promotional activity retreats for the first time in five weeks. USDA says 8.767 stores have butter deals this week, down 23% from the week before and 6% year-over-year. Average price comes down, though: $3.56 per pound, down 21 cents on the week and down 23% year-over-year. A total of 11,837 stores will feature six-to-eight-ounce cheese shreds, down 7% on the week but up 15% year-over-year. Prices come down sharply, though, with the average at $2.16 per package, down 36 cents on the week and down 3% year-over-year to the lowest level since July 2024.

Futures and options on futures trading involves significant risk and are not suitable for every investor. Information contained herein is intended for informational purposes and is obtained from sources believed reliable but is in no way guaranteed. Past results are not indicative of future results. Any data contained herein is proprietary and may not be copied, disseminated, or used without the express written permission of Ever.Ag Insights.