The Scoreboard

Comment

Last week, we learned that… US food sales remain stagnant. Whether it’s the economy, the rising use of GLP-1 medications, a flat-lining population, or some combination, Americans aren’t buying much more food than they were a year ago. The latest Retail Sales report from the US Census Bureau reinforces the point.

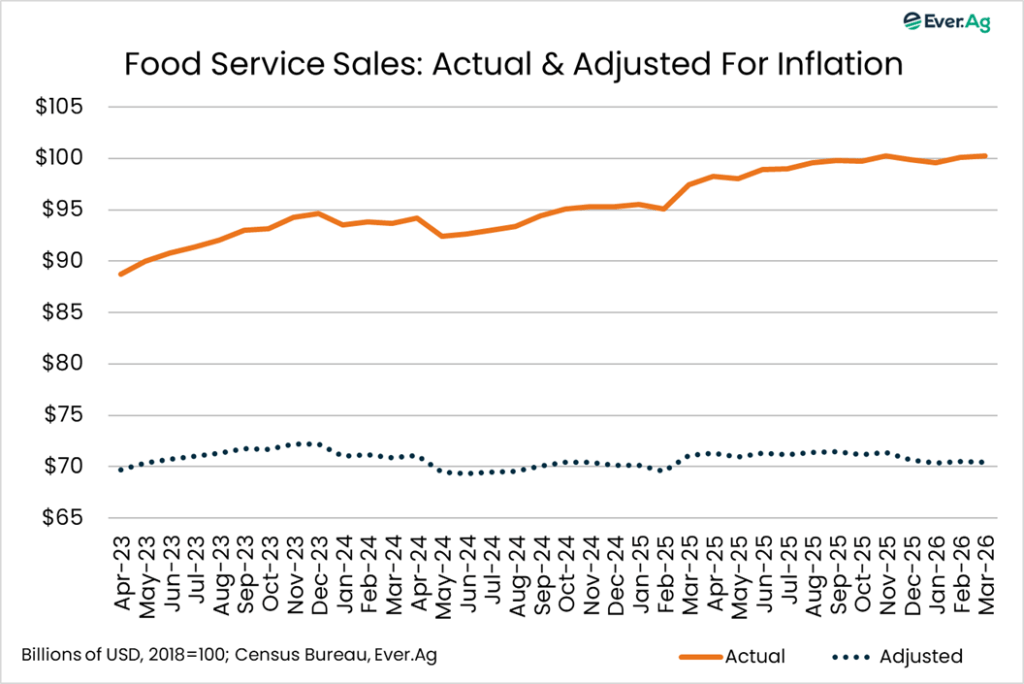

Grocery store sales totaled $76.3 billion in March, up just 0.5% year‑over‑year, well behind food‑at‑home inflation (+2.0%). Food service sales rose 2.8% to $100.2 billion, also trailing inflation (+3.8%). Adjusted to 2018 dollars, both channels are moving backward. Food service sales fell 0.9% year‑over‑year (the worst showing since February 2025), while grocery sales dropped 1.4%, marking four consecutive months in negative territory.

Looking back three years, food service sales are up 13.3% in nominal terms but only 1.0% in real terms; grocery sales are +4.4% nominal and ‑1.1% real. The takeaway is clear: whatever the mix of causes, consumer demand remains a headwind for grocery, CPG, restaurants, and, by extension, food and agricultural commodity markets, and isn’t likely to turn into a tailwind anytime soon

* * *

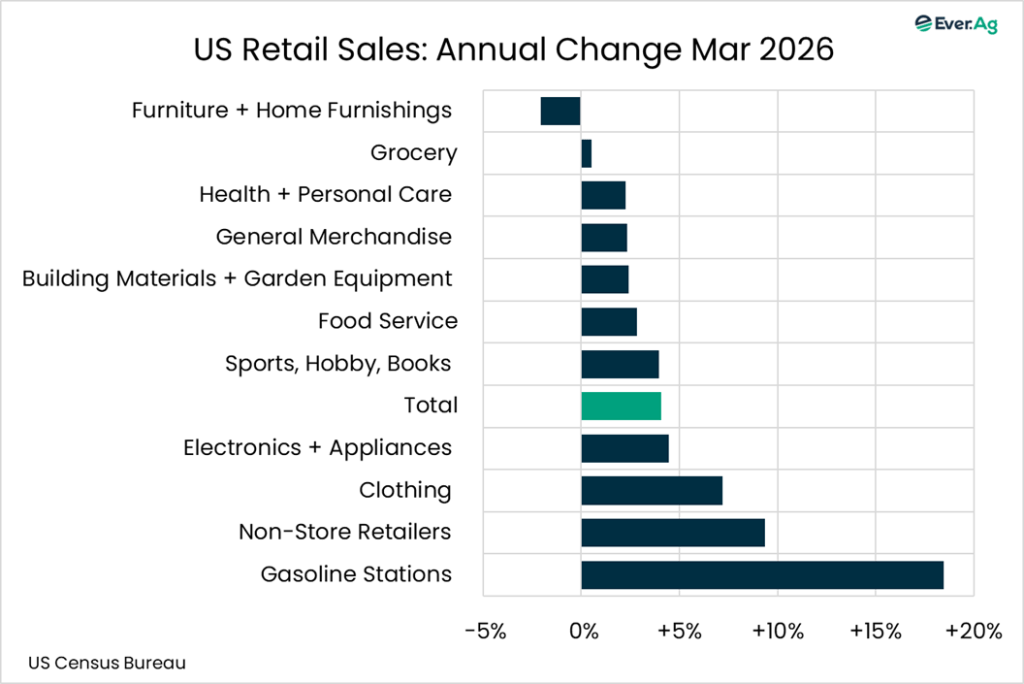

US retail sales in March topped expectations, but higher gasoline prices did most of the work. Sales totaled $752.1 billion, up 1.7% on the month and up 4.1% year-over-year. Analysts expected +1.4% month-over-month. Gasoline station sales increased 15.5% month-over-month and 18.5% year-over-year. Retail gasoline station sales accounted for 8.1% of total sales, up from 7.1% in February and the biggest share since March 2023. Other standout areas: non-store retailers (online merchants) and clothing (+7.2%).

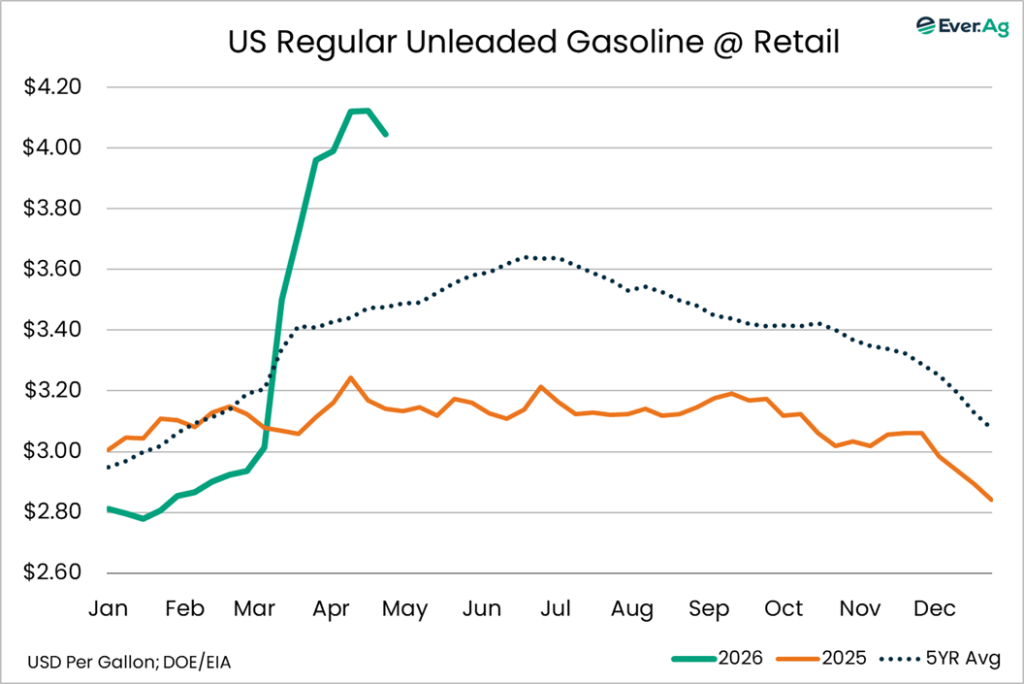

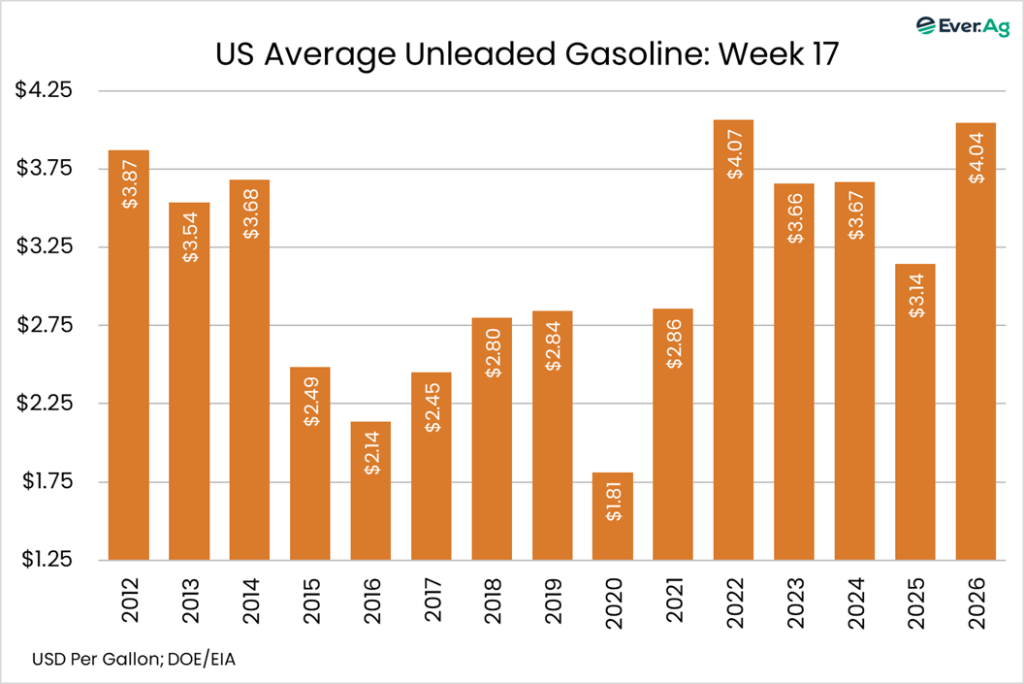

In the near term, gasoline prices have stabilized, even at elevated levels. The American Automobile Association reported regular unleaded at $4.09 per gallon, up three cents on the week.

* * *

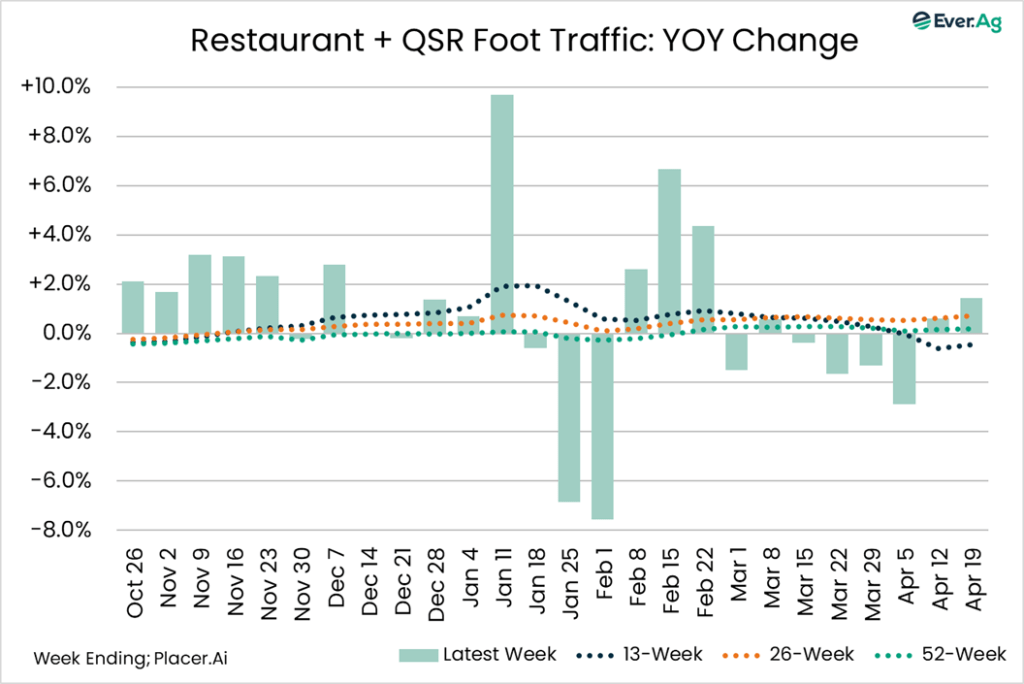

While restaurant sales aren’t robust, traffic hasn’t collapsed yet in the face of higher gasoline prices. In fact, Placer.ai data shows small gains recently. For the week ending April 19, restaurant foot traffic increased 1.1% year-over-year, with QSR activity up 1.5%, making for a combined advance of 1.4%, the best showing since mid-February. This is resilience, not strength — but it counts for something.

* * *

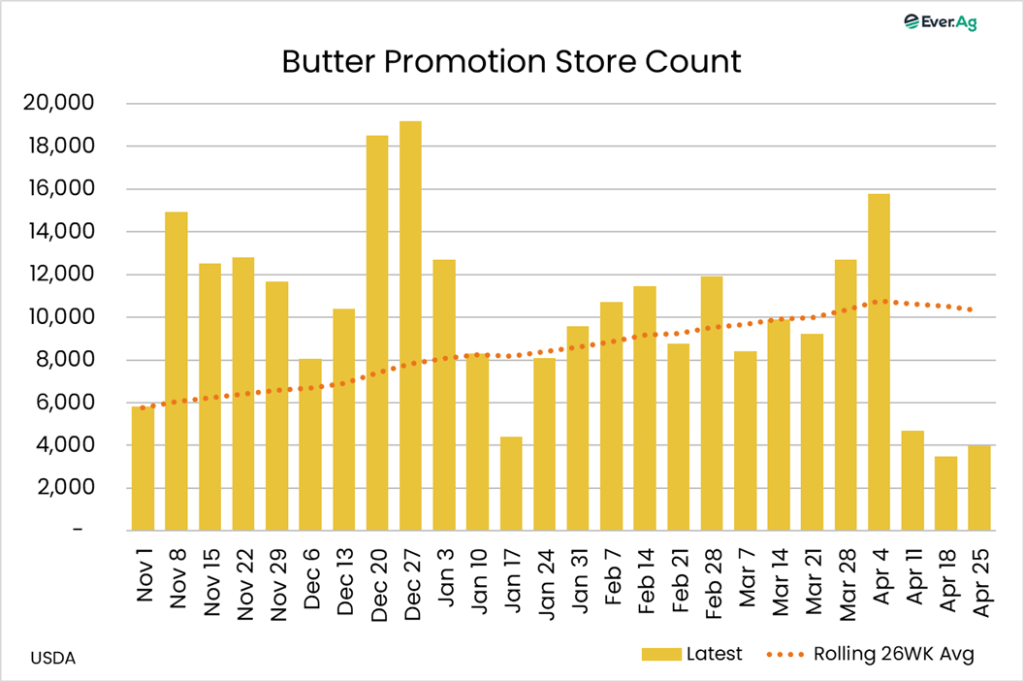

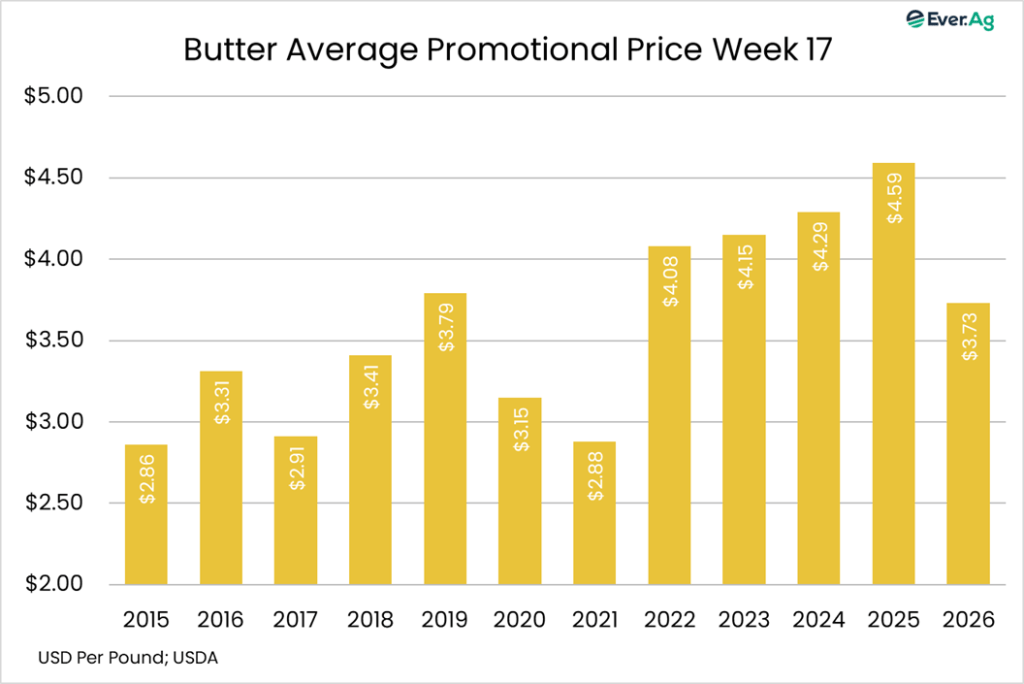

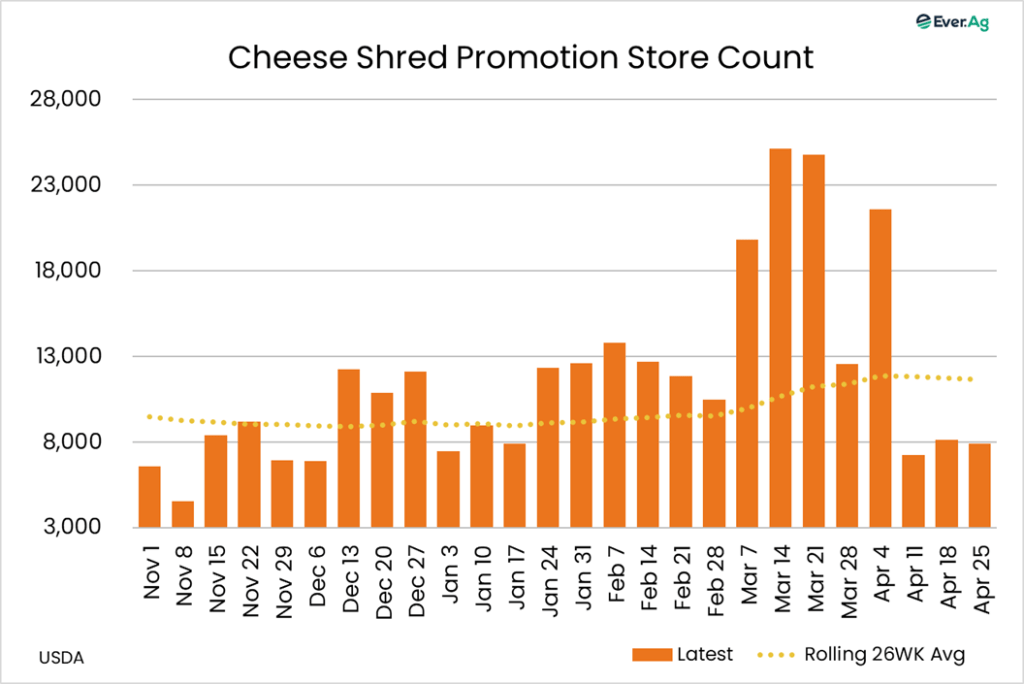

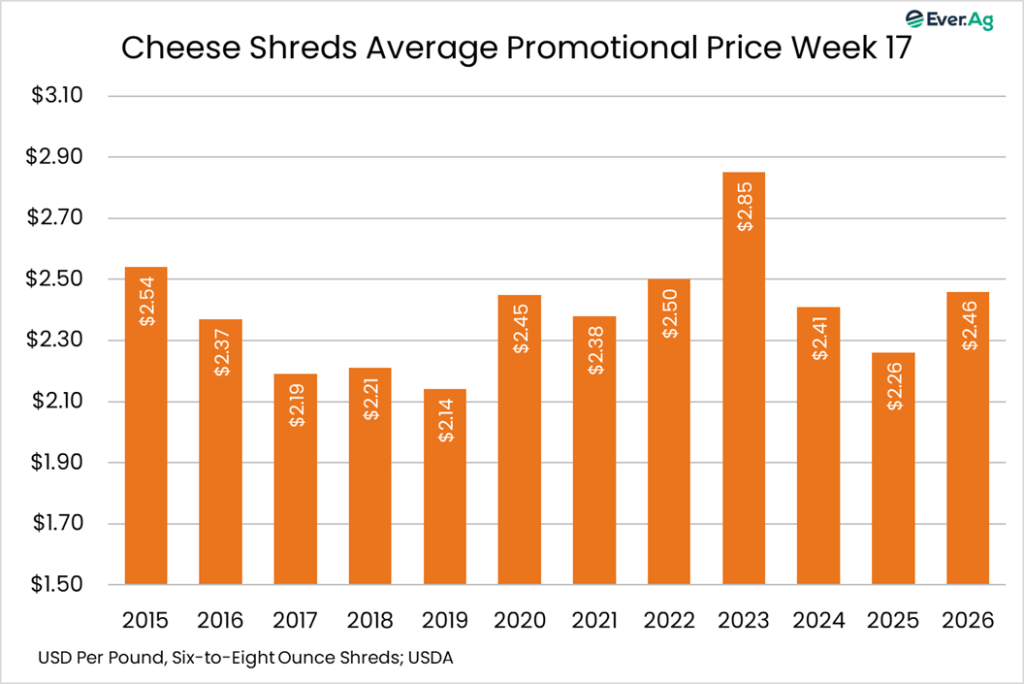

We’re in week two of the promotional lull for butter and cheese. According to USDA data, a total of 3,982 retailers have deals on butter for the week ahead, up 14% from last week but way below the rolling 52-week average of 8,072. The average price dropped back to $3.73 per pound, down 14 cents on the week and down 19% year-over-year. Six-to-eight-ounce shredded cheese promotions drop to 7.898 outlets, down 3% on the week and below the 52-month rolling average of 10,721. Average price: $2.46 per package, up 27 cents on the week and up 9% year-over-year to the highest level in five weeks.

Futures and options on futures trading involves significant risk and are not suitable for every investor. Information contained herein is intended for informational purposes and is obtained from sources believed reliable but is in no way guaranteed. Past results are not indicative of future results. Any data contained herein is proprietary and may not be copied, disseminated, or used without the express written permission of Ever.Ag Insights.